Welcome to the website for the Real Incomes Approach to Economics!

The Real Incomes Approach has evolved since I initiated its development in 1975, in Rio de Janeiro, into the only macroeconomic policy with a direct microeconomic foundation and that is wholly supply side. In 1976 my focus in its development moved from Brazil to the UK economy and to this day its development continues with a focus on the UK economy.

What emerged as "supply side" economics, in the late 1970s was no more than a fiscal device which, in practice, failed. The recognition of supply side being the issue to resolve slumpflation was correct at the time but the solution was moulded in the light of existing, proven-to-be-ineffective, policy instruments so this did not resolve the issue. As a result there was a good deal of suffering imposed by the policy solutions. I was not involved in the development of "supply side economics" and was surprised when I reviewed it in early 1980s to find that it has very little to do with supply side; it is an Aggregate Demand Model (ADM) fiscal policy. So why it has that name remains a mystery. My own view on what supply side should be is easy to understand and can be found here: What are the elements of a supply side policy?

My motivation for initiating the economic analysis, that ended up as the Real Incomes Approach, was that having studied post-graduate economics and both Cambridge and Stanford Universities I found that, in 1975, when I tried to work out a solution to slumpflation I was unable, with my understanding of the existing policy instruments, to find one that I found to be acceptable. All options would cause serious prejudice to segments of the economic and social constituencies. I therefore set about investigating why conventional economic theory and practice was so constitutionally defective. I found it unacceptable that poorly conceived socially destructive policies, which hardly passed for experiments, could be called "essential medicine" for economic recovery involving national constituents. Unfortunately this blunderbuss mindset persists today in many politicians and many economists around the issues that are referred to as "austerity" and "living within our means". The dyed in the wool "there is no alternative" mantra continues. This conveys an inability to observe what is happening or to acknowledge and accept the evidence that the theory does not translate into practice in an effective fashion. This reflects an intellectual deficit and a worrying level of ignorance of the economic and financial options that are superior to what passes for conventional macroeconomics with its threadbare tool kit of currently available policy instruments.

In reality Keynesianism, monetarism and supply side operate using different perspectives on a common but flawed ADM (Aggregate Demand Model) paradigm which I refer to as KMS policies. So the electoral cycles that result in each false option coming to the fore and applied and then, inevitably, failing, is a wholly predictable disruptive cycle that is unacceptable.

This website was set up to disseminate information on the Real Incomes Approach and to help clarify some questions and hopefully encourage feedback on this topic. The Real Incomes Approach remains work in progress.

If this is your first visit to this site, I would encourage you to read the Introduction page. This provides a broad sweep of the breadth of impact that a Real Incomes Approach to policy can have and, hopefully, this will encourage you to read further or at least ask questions. This site contains a selection of about 200 of the more recent articles and documents from the archive, accessible from this page, including the most recent output.

I have recently opened the Botequim where I explain the context of the most recently posted articles providing backgrounds. I welcome constructive feedback that might point to any flaws that reader might detect in this approach.

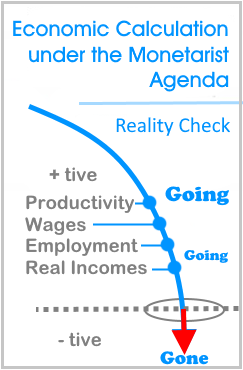

The United Kingdom and other countries, under the weight of KMS policies, are experiencing an inversion in real growth in the context of the world's declining natural carrying capacity. Recent assessments indicate that climate crisis actions are still inadquate. My contention is that this is a direct result of the inappropriate macroeconomic policies pursued for some time. In particular, these have not provided the appropriate incentives on the supply side to bring about necessary change to more appropriate sustainable technologies and techniques. The last attempt at an "adjustment" or "improvement" to KMS policies was the introduction of quantitative easing (QE) introduced to "recover" from a KMS policy-induced financial crisis in 2007/2008. However, this has resoundingly failed by exacerbating income disparity and overall levels of debt now being greater than in 2008. Real incomes, for an increasing proportion of population, continues to follow a downward trend. Productivity-enhancing investment has declined.

The Real Incomes Approach is an attempt to address this type of prejudice associated with KMS policy cycles and to establish the fact that "there is an alternative". Any feedback that helps improve its theoretical coherence and applications feasibility is welcomed as contributions to the improvement in its utility as a realistic option to failing KMS policies.

Hector McNeill

SEEL - Systems Engineering Economics Lab

Portsmouth

hector.mcneill@realincomes.org.uk

Telephone: +44 (0) 7 760 444 625.

|

|

|

RIP is based on the Real Incomes Approach to Economics. RIP provides a sustained productivity incentive system that benefits any size and supply side production company in any sector from agriculture, industry, manufacturing and logistics. It lowers the risk of using efficiency-enhancing investment to secure competitive prices enabling companies to lower or even eliminate inflationary output.

RIP is based on the Real Incomes Approach to Economics. RIP provides a sustained productivity incentive system that benefits any size and supply side production company in any sector from agriculture, industry, manufacturing and logistics. It lowers the risk of using efficiency-enhancing investment to secure competitive prices enabling companies to lower or even eliminate inflationary output.

giving primacy to economic arguments in their justification for their offhand treatment of others. So why in a democracy do people have no recourse against such abuse?

giving primacy to economic arguments in their justification for their offhand treatment of others. So why in a democracy do people have no recourse against such abuse?

(1908-1986)

(1908-1986) Annoucement

Annoucement

Real Exchange

Real Exchange

Reducing the negative

Reducing the negative