This note is part of a series as a sequel to the article, From nominal growth to stable real incomes. To place this note in context readers are encouraged to read this article before reading this note.

This short note is to explain a simple reality of why the so-called "transitory" inflation is a permanent feature of what constitutes monetary policy today.

What is the real incomes trap?The real incomes trap is a decline in the purchasing power of wages, or real incomes, created by financialization and intensified by quantitative easing.

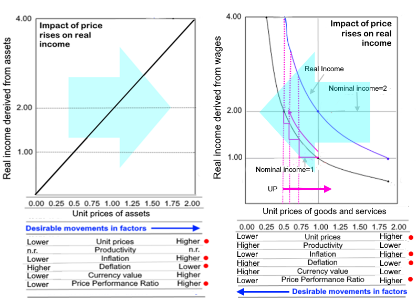

The salient impact of QE is a rise in asset prices which is very much to the benefit of those who earn their income from asset dealing and holding. The note

"RIP and real wages" presented two diagrams to explain why the interests of wage earners and asset dealers are represented by diametrically opposed movements in prices of goods and services, on the one hand, and asset prices on the other. This fact is indicated by the turquoise arrows in the diagram on the right. To examine the detail please refer to the original note.