The Real Incomes Approach applies the logic of the Say modem in a

"Production, Accessibility and Consumption Model". Notice the term "accessibility" that refers to accessibility of prices in relation to disposable incomes as well as local availability and support to products and services.

In terms of a macroeconomic policy the policy instruments provide a direct incentive for economic entitles to stimulate consumption through competitive prices rather than through pumping volumes of fiat currency into the economy raising debt.

This price performance policy is the only macroeconomic policy proposition that recognises the

"calculation and knowledge problem" and distributes the determination of the main policy instrument values to economic entity and workforce levels enabling refined optimization of production throughout the economy.

Replacing "planning" with a proactive competitive economyPlans are an attempt to map out desired future pathways and transitions. However, because all economic entities are different in all critical and general factors of performance the attempt to achieve "centralized plans" encounters a wide range of impediments and constraints because central planning cannot manage the "

calculation and knowledge problem" which can only be addressed by each entity in response to their particular circumstances. This means central plans impose varying levels of risk on companies.

To solve the risk, calculation and knowledge issues the Real Incomes Approach devolves the manipulation of policy instruments to the level of economic entities in a way that is advantageous to companies in any state of circumstances. This is achieved by encouraging competitive price setting against productivity enhancing investment through an incentive scheme. This augments immediate profits to the degree that unit prices kill inflation while penetrating the market and enhancing the general state of real incomes. The general state of real incomes signified real income of companies and purchasing power of consumers. In other words rather than a fixed plan the economy is managed through a set of targets for the future performance of corporate

PPR-price performance ratios. The PPR provides an indication of the degree to which the supply chain individual firm activities impact real incomes as a result of the summation of unit input costs (transacted) and the unit output prices (transacted). This occurs across a transformation process including: input procurement (transaction), external input logistics, internal input logistics, transformation process, internal output logistics (product or services), product sales (transaction), external output logistics (product or services) and delivered product or service.

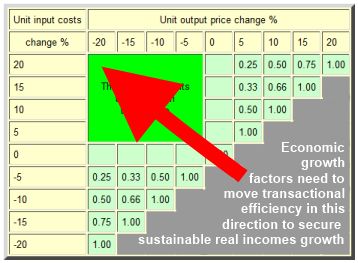

Innovation target zonesWith current technology, techniques and accumulated tacit knowledge, there is a frontier beyond which we cannot operate with state of the art technology (See:

Tacit & explicit knowledge). For example if unit input costs rise by 20% it would normally be difficult to secure an immediate 20% reduction in unit output prices without losing a considerable amount of money. However, through re-adaptations of state of the art, systems engineering and rational decision analysis it is usually possible to redesign processes and maximize process throughput so as to accelerate the evolution of technological and economic performance. In this way it is possible to enter the innovation target zones. This leads to a significant rise in supply side-generated real income as a result of lower unit prices and market penetration. The innovation target zones, desirable and undesirable states are shown in the table below.

Price Performance Ratios (PPRs)

associated with different unit input value movements & movements in unit output prices

| Unit input costs | Unit output price change % |

| change % | -20 | -15 | -10 | -5 | 0 | 5 | 10 | 15 | 20 |

| 20 |

This area represents

the innovation

target zone | 0.00 | 0.25 | 0.50 | 0.75 | 1.00 |

| 15 | 0.00 |

0.33 | 0.66 | 1.00 | |

| 10 | 0.00 | 0.50 | 1.00 | | |

| 5 | 0.00 |

1.00 | | | |

| 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | | | | |

| -5 | 0.25 | 0.33 | 0.50 | 1.00 | | | | | |

| -10 | 0.50 | 0.66 | 1.00 | | | | | | |

| -15 | 0.75 | 1.00 | | | | | | | |

| -20 | 1.00 | | | | | | | | |

Innovation target zone | | Desirable states | | Undesirable states | |

|

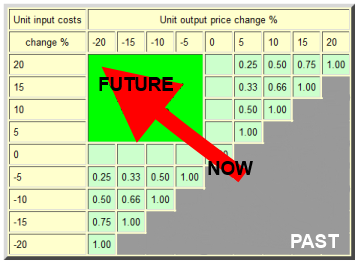

This table provides a map of the distribution of likelihoods of sources of enhanced real incomes. However, the extent of real income generation at the macroeconomic level can only be estimated by applying sector demand schedules for local and regional markets. In the case of global markets, the elasticity of demand for price-setters is well above the market norm so the returns to lower PPR states are enhanced by market penetration, returns to scale, better procurement conditions and the accumulation of tacit knowledge leading to quantifiable increases in performance measured in terms of unit costs of production.

The PPR map is not only a useful guide to feasible attainment in terms of real income growth according to the sector/technologies but it also provides a map of targets for research and development and technology requirements. At all times these explicit descriptions will be improved, in practice, through the refinement of techniques, that is, the way people apply technology, achieved through practice and the further accumulation of tacit knowledge. The PPR map also provides an indication of the evolutionary transition of where we stand today in terms of the given past and the necessary future.

Why the Real Incomes Approach is different>

The Real Incomes approach makes use of such factors as critical policy and business rule resources. It makes use of them by influencing transactional behaviour to stimulate the proactive application of these growth factors. It is notable that the main conventional texts on Keynesianism, monetarism and supply side pay scant attention to these factors and as a result provide no basis for gaining traction and real economic growth when attempts are made to apply these theories as policy.

The incentive to encourage increased competition associated with lowered riskThe incentive for decisions that support the general national objective is a

PPL-price performance levy. The levy is a withholding levy where rebates, or levy reductions, are proportional to the price performance ratios achieved. These should be set to enable efficient companies (those with low price performance ratios) ending up paying no levy at all.

The logic of this free flowing system is that there will always be a future desirable PPRs and the way to achieve them in a reduced risk manner is to improve technologies and techniques to secure more for less and thereby reduce the pressure on resources.

Population and behaviourOur main issue remains excessive population growth combined with behaviour and habits that extract too many resources and with the excuse this is to feed the future generations of an expanded population. This is illogical and family planning techniques need to be made more widely available to enable people to change behaviour. The most striking example of population control being a success story in terms of pulling more people out of poverty was that of China that adopted the one child policy in the 1980s after an assessment of the limits of growth".

FinanceThe Say model and the Real Incomes Approach does not rely on loans and debt to secure "growth". As soon as an economic entity develops a competitive level of operations, the monetary savings resulting are often sufficient to begin to invest marginal improvements so, improvement feed on improvements. The other options is mutual arrangements where a group work as employed in their own company and share saved margins to improve their performance. Price performance policy assists this trend by ensuring efforts at increased performance either through investment and or price setting can result in immediate levy reductions thereby reducing risks.

The financing option of loans and debt is at all time risky with around 30% of all projects failing and companies losing their assets to financial entities. This level of transfer of ownership of assets is recorded as part of he success of the financial sector while in reality it represents a loss to the productive sector. Amongst the "solutions" advocated by the financial interests is increased Carbon trading which to date had not achieved any improvements in temperature rises. COP26 was informed that the carbon price it too low. No one really knows because of the calculation and knowledge problem linked to intentionally exaggerated carbon capture estimates combined with intentionally underestimated emissions estimates. This system is far from transparent but remains a convenient way to earn commissions. The financial sector is the closest to central banks and they are also the main sources of funds for political parties and the media. They wish to continue business as usual but relabeling their modus operandi as a green initiative. The aggregate demand model needs to be replaced with the production, accessibility and consumption model and this signifies a need to introduce price performance policy.

1 Hector McNeill is director of SEEL-Systems Engineering Economics Lab

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2021) unless otherwise indicated