Natural returns & state imposed calamityDepending upon the activity, state of the art technology and techniques the appropriate levels of interest rates for any economic unit to justify investment will depend upon the expected return on the investment. The ideal situation is one where interest rates fall into a range below the potential returns on investment to make more investment feasible.

In 1898 Johan Gustaf Knut Wicksell (1851-1926) published an important work entitled: "Interest and Prices" where he identified a natural rate of interest and the money rate of interest. The money rate of interest was that operating in capital markets and natural rate of interest was that at which supply and demand in the real market was at equilibrium with the interest rate being the "equilibrium price for money".

This raised the question as to the need for capital markets.

If the natural rate of interest was not equal to the market rate, then the demand for investment and quantity of savings would not be equal. If the market rate is lower than the natural rate, then companies are encouraged to invest and economic expansion occurs.

NEGATIVE IMPACTS OF MONETARY POLICY

ON GROWTH & PRODUCTIVITY

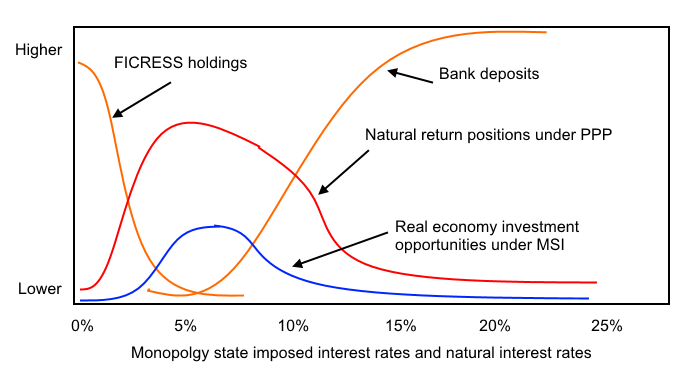

MSI: monopoly imposed interest rates;

PPP: under real income natural rate Price Performance Policy |

|

The natural rate is the return on capital, that is, the real profit rate equivalent to the marginal return on new investment. The money rate is the loan rate fashioned by the bank and credit becomes "additional money". Indeed, as was finally admitted by the Bank of England recently

2 (see

"Money creation in the modern economy - Bank of England" Quarterly Bulletin 2014 Q1) bank credit creates deposits which can be used by borrowers and therefore the bank creates money and increases the money volume in the economy.

In reality the main policy instrument of government via the Bank of England is interest rate-setting. As described in the text on the left this policy has been somewhat calamitous because interest rates seldom fall to a reasonable level to come below the natural interest rate, and, when well below that rate, money, as in the case of quantitative easing which it totally designed to benefit the banks, funds take flight into assets starving investment activities.

In the diagram above the orange lines show the "drainage" of investment funds from productive investment in association with high or very low interest rates with the real opportunities for investment (and therefore increased productivity, exports and import substitution) being the unimpressive blue line on the graph. The Real Incomes approach, having constitutional economic foundations does no permit the state to impose arbitrary interest rates but encourages investment and investment opportunities around the natural return scales according to sectors and sub-sector practice and future potential. This more robust source of growth is indicated by the red line.

2 For the last 50-60 years leading macroeconomic textbooks did not admit that banks create money this way but insisted on a mumbo-jumbo linked into the unconvincing logic of the Quantity Theory of Money (see

Real Incomes & the Quantity Theory of Money).