Why Real Incomes?

Hector McNeill1

SEEL

This is the third rewrite of this article. This has been prompted by the content of the considerable feedback on the topic of real incomes. To some degree queries arise as a result of lack of clarity on my part but more often because of a sparse appreciation of what the indicator real incomes signifies in terms of the critical variables that determine its construction or destruction.

On the other hand, another reasons for this rewrite is to cover aspects which were not referred to previously which have become more evident as significant issues requiring policy and programme solutions. In this context I refer to the 2015 launch of Agenda 2030 and the Sustainable development Goals. These establish nation wide indicators for human wellbeing across many domains defined in terms of 17 Sustainable Development Goals and over 200 indicators. I expand on these issues in this article. These establish nation wide indicators for human wellbeing across many domains defined in terms of 17 Sustainable Development Goals and over 200 indicators. I expand on these issues in this article.

There is a tendency for people to get lost in the technical detail of the variables that make up the way to measure real incomes as a compound index, rather than focusing on why I feel real incomes is one of the more important indicators and economic policy objective. I therefore start this rewrite by explaining what real incomes is and then follow this up with the technical aspects.

I think the feedback received does point to the lack of attention paid to this topic both in the teaching of economics as well as in commonly applied analytical techniques.

In this article I have attempted to add clarity where required and to provide a more detailed exposition on the interactions of key variables in contributing to the status of real incomes. Using this indicator for economic growth can release macroeconomic policy from the grips of the aggregate demand model that requires monopolistic centrally determined state directives of single values for policy instruments of arbitrary relevance to a diverse social and economic constituency.

|

Critical variables that determine real incomes

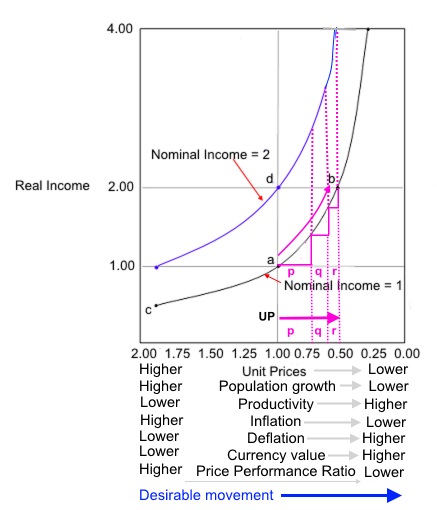

Real incomes are usually defined in terms of nominal incomes and the levels of unit prices. Variations in real incomes relate to changes in unit prices which can be expressed as inflationary or deflationary, to determine any gain or loss in the purchasing power of some nominal income. Macroeconomic policy needs to be concerned with securing sustained improvements in the standards of living of the country over extended time horizons. This fact changes the complexion of real incomes. If policy becomes directed towards sustaining or increasing economic growth based on the indicator of real incomes then the consideration of price variations need to transition from being passive observations of events in the market to a better understanding of feasibility of influencing price changes through policy. The feasibility, effectiveness and efficiency of policy in helping raise real incomes depends upon an ability to provide incentives to encourage price reductions. However, the feasibility of achieving unit price reductions in each economic unit can only be assessed on the basis of knowledge of the operational performance potential of the specific technologies and techniques deployed. Policy cannot identify where and how productivity can be improved, this is the function of company management. However, policy can provide economic units with larger degrees of freedom in their setting of output prices. The diagram on the right shows the dependency of real incomes on productivity and unit prices and the value of the currency (purchasing power). As can be seen a movement from point "a" in the diagram to increased real incomes can be achieved through unit price reductions. So in the case of point ""a" real incomes can be doubled by halving unit prices and the movement to point "b". Note that in this case nominal incomes remain at 1.00 while real incomes increase from 1.00 to 2.00. The nature of the process of attainment of unit price reduction is that this is normally a gradual process made feasible by increasing productivity in terms of technology, experience and the accumulation of human tacit knowledge (See: Tacit & explicit knowledge). Therefore the halving of unit prices would follow gradual steps such as those traced by the price reduction decrements of "p", "q" and "r". At the level of the firm and the macroeconomy the best indicator that things are moving in the right direction is the price performance ratio (PPR) (See "The price performance ratio"). If unit output prices are contained or reduced in the face of increasing input costs, the PPR declines and this is a convenient indicator that is able to reflect the combined benefits of higher productivity, lower unit prices and stabilization or increase in currency purchasing power. The decisions on where productivity can or should be increased is, however, not the domain of policy but rather that of the management of economic units. Policy should, however, facilitate decisions to increase productivity by helping reduce operational risks associated with decisions to stabilize or reduce unit prices. Currently conventional policies constrain increases in productivity as a result of the profit paradox, methods of government revenue seeking and inappropriate audit and accountancy standards. The outcome is corporate tax avoidance and evasion on an increasing scale, falling government revenues, declining productivity and a decline in the value of the currency and real incomes (wages). | |

|

|

What is real income?In a who dunnit book there are those who are so curious that they will read sections of the final chapter to find out who did it. They are then left with the problem of finding out why he or she did it. So in this article I will state up front why, we already know the guilty party is real incomes.

Conventional Keynesian, Monetarist and Supply side (KMS) policies apply across the board state monopoly centralized interventions in markets by interest rate-setting, taxation rate-setting and often by raising government debt implying higher taxation at some later date or reductions in public service provisions if debt has become excessive. These monolithic policy interventions impact the interests of a diverse social and economic constituency who have very different needs, capabilities and access to resources. As a result KMS policies generate winners, losers and those who remain in neutral policy impact states. It is virtually impossible to achieve a state of positive system consistency and therefore policy traction is low (see positive systemic consistency).

Today, there is a significant paradox in the economies of the United Kingdom and United States. This is that during the last 30 years the state of inequality, measured in terms of income, has increased. In some cases the relative level of inequality approximate the levels in some low income, albeit at higher levels of income. One of the principal Sustainable Development Goals is number referred to as "reduced inequalities". Development economics addresses this sort of problem and the more extreme ineuqlity is the more difficult it is to initiate growth. Indeed, because of the failure to address the specific issues of inequality, the performance of Agenda 2030 appears to be floundering2. A recent report indicates that Agenda 2030 is also failing to bring about positive results in the domains of responsible consumption and production and climate change i.e. implementing change stragies to combat this phenomenon.

The policy challenge

The human suffering associated with the different and many economic crises that have accompanied KMS policy decisions is unacceptable and this is why work was initiated on the Real Incomes approach. KMS policies make use of a range of policy instruments designed to influence specific policy targets such as growth, nominal output, aggregate demand, unemployment, inflation, exports, imports, import substitution and exchange rates. None of these variables has any substantive significance to the management of economic units who need to allocate resources to maximize operational returns. There is therefore no coherence between macroeconomic policy targets and the objectives of each company. In order to tackle this problem of differential policy impacts and companies surviving, almost in spite of macroeconomic policies, there is a need to identify microeconomic objectives that are aligned directly with macroeconomic objectives.

So this is why the Real Incomes development programme was initiated.

Real incomes

The track record shows that KMS policies make use of single variable indicators resulting in an inability to control other variables and therefore predict the outcome of determinants that can reduce the effectiveness of policy (see The Tarshis paradox). What is required is a compound index or variable whose value is a measure of benefit to the social and economic constituencies and that is determined by a collection of variables which contribute to the compound variable's value and whose contributions can be influenced by policy. The best measure or indicator of economic success at both the macroeconomic and microeconomic level is real incomes. This fact was identified in 1976, within 12 months of an economics research and development programme starting and this finding resulted in the programme gaining its name. However, not forgetting our objectives which include:

- the identification of a macroeconomic theoretical model with microeconomic foundations

- maximizing the coherence between macroeconomic and macroeconomic objectives

- bringing about a state of positive systems consistency in policy outcomes

- providing management of enterprises with coherent business rules that maximize their economic objectives and contribute directly to macroeconomic objectives

- enabling the free operation of economic units to optimism operations without policy-induced constraints

- augmenting policy traction

In the Real Incomes Approach development programme a considerable amount of time has been dedicated in understanding the implications of using real incomes and coming up with policy propositions on how this can work in practice. One of the most significant results has been the need to reject of the Aggregate Demand Model of the economy upon which KMS policies are founded to substitute this with the Production, Accessibility and Consumption (PAC) Model of the economy (see The PAC Model of the Economy)

The conventional indicators of growth, nominal output, aggregate demand, unemployment, inflation, exports, imports and exchange rates can, and often do, move in mutually contradictory fashions when the main policy is confined to the use of the conventional instruments of money supply and interest rates, government taxation, expenditure and debt.

Under conventional regulatory frameworks the profit motive is often stated to be the motivational force for economic activities. Indeed, the Aggregate Demand Model is largely justified on this basis. However, the profit motive does not operate as predicted but the general policy framework generates perverse incentives that encourage tax avoidance and evasion, the hiding of shareholder incomes, reducing government revenues and by imposing severe constraints on wages - see the profit paradox. In addition to this paradox there are two more policy domains that contribute to extreme inefficiency and these are monetary policy (see The monetary paradox>) and fiscal policy (see The fiscal paradox).

Therefore a Real Incomes policy not only has to contend with substituting currently key pillars to KMS policy but also needs to eliminate the impacts of the profit, monetary and fiscal paradoxes all of which make optimized resource allocation at the level of the firm virtually impossible. The ways and means Real Income policy achieves this is contained in other articles.

The significance of real incomes as a policy objective

Real incomes are a compound variable because they are determined by the interaction of the following variables (determinants):

- nominal incomes and their movements

- unit output prices and their movements

- productivity

- price elasticities of consumption

- the real income multiplier

- investment in technology and human resources

Therefore the monitoring of real incomes can be used to determine which of the determinants need to be influenced to sustain real incomes. In order to build a practical real incomes policy it is essential that the macroeconomic policy objective of sustaining or increasing real incomes be the same objective adopted by economic units, shareholders and the workforce. By aligning macroeconomic and microeconomic objectives on the basis of a single indicator, real incomes, the overall macroeconomic model achieves a microeconomic foundation and transparent operational coherence.

The essential value of this model is that it enables economic units to freely allocate resources to maximize their real incomes according their own objectives, capabilities and access to resources. Thus Real Incomes policy operations are largely bottom up as opposed to the centralized state monopoly interventions of conventional policies that create winners, losers and those unaffected by policy. This extreme policy differentiation is caused by the natural diversity and conditions of the social and economic constituencies which conventional policies are not designed to accommodate.

For this to work such operational decisions must remain with corporate management who are more aware of the potential and limitation of their economic unit. In principle these decisions should not be determined by state decrees acting through central banks on interest rates and money volumes or arbitrary taxation and levies or attempting to influence demand through public expenditure based on debt.

As long as the microeconomic objectives and macroeconomic objectives are aligned in the form of real incomes then the function of policy is to facilitate microeconomic decision-making and resource allocation by providing incentives for investment in technology and human resources and the gradual lowering of unit prices as a result of increased productivity, thereby increasing real incomes.

All productivity issues can be resolved directly as a result of supply side microeconomic decisions that determine technology and human resources allocation, innovation, learning and the accumulation of tacit and explicit knowledge. For conventional economic theory and practice including Keynesianism and Monetarism and, indeed, supply side economics, these central roles of these factors are represented by blank pages.

It is more than evident that real incomes management at the level of the macroeconomy requires an intimate relationship between microeconomic decisions on resource allocation and the objective of achieving higher real incomes. This objective is very difficult to achieve using conventional fiscal and monetary instruments, government revenue seeking methods and the regulatory accounting and audit frameworks. Each of these impose conflicting constraints on companies leading to sub-optimal levels of productivity.

Under Real Incomes Policy and Price Performance Policy (PPP) in particular (See "Bare bones PPP") use is made of the policy instrument Price Performance Ratio (PPR) which is manipulated by corporate management on the basis of an incentive to raise returns based on productivity increases (See "The price performance ratio"). The productivity bonuses arise from rebates on Price Performance Levies that decline with a falling PPR value (reflecting higher price performance productivity) (See "Price Performance Levy"). The final PPL paid and size of rebates is wholly dependent upon management decisions at the level of the firm. Therefore the Real Incomes Approach and PPP avoids the ineffective conventional approach consisting of monopolistic state market interventions that lack incentive and therefore traction (See The Real Incomes Approach - The main theoretical principles & policy options).

Since 1945 the Bank of England actions have resulted in a reduction of the purchasing power of the pound to something like 2% now and the UK trade deficit is now the highest in our the history in real terms (2015). Continual devaluation, in an undeclared international currency war, under quantitative easing and low interest rates will never secure higher exports without effective gains in productivity. Monetarism is based on a very weak theoretical model (QTM-Quantity Theory of Money) that does not support the real economy and cannot support a real incomes policy - see Real Incomes & the Quantity Theory of Money.

The most significant characteristic of real incomes is that they can be raised without using any of the conventional policy instruments that rely upon centralized monopolistic state interventions using arbitrary levels of interest rates, taxation or government debt to influence so-called aggregate demand. Real incomes, combining productivity, unit price setting and currency stability, can be raised by applying supply side decisions shaped by the specific circumstances and potential of each economic unit. Real Incomes policy avoids the imposition of inappropriate levels of interest rates and taxation on firms. Therefore the primary lead impact of Real Incomes policy is to encourage firms to contain inflation on the basis of productivity and price-setting on a beneficial basis. This being to the direct benefit of each economic unit helps sustain policy traction, something lacking from conventional policies. A further explanation of the limitations of the conventional aggregate demand model can be appreciated by referring to the article,"The PAC Model of the Economy".

Growth in the economy

One of the impacts of a downward trend in unit prices and rising real incomes is that the economic growth multiplier rises because the propensity to consume rises as a result of higher price elasticities of consumption. The current crisis which under KMS policies is experiencing anaemic growth rates that are even being baptized as "recovery" when the UK economy has yet to regain its 2007 levels of operation, is the direct outcome of a failure to address properties of the income multiplier. Further explanation on this important fact can be found in the article "The Real Growth Multiplier". In order to understand how real incomes policy can initiate the impulse for sustainable growth in real incomes (something plaguing most economies today) see the article "Growth impetus".

Growth in positive trade balance

A notable failure of monetary policy in the UK has been that the impact of centrally imposed interest rate cycles associated with the desire to control inflation. The impact of these cycles has been for productivity to fall as a result of deficient investment. The UK balance of payments has become increasingly negative in spite of the fact that the value of the pound has constantly declined since 1945 as a direct result of the 2% inflationary target which devalues the pound by over 18% each decade.

The balance of payments can be more effectively managed on the basis of Real Incomes policy where increasing productivity can result in stable or lower unit prices while the value of the currency is maintained resulting in lower rates of devaluation or stability. In the end productivity and pricing will determine the degree of import substitution and exports according the price elasticity of consumption in foreign markets. In a recent exchange between Mark Carney, the governor of the Bank of England (BoE), and the Parliamentary Financial Committee he expressed the opinion that exchange rates remained "free" and were not a consideration for the BoE. However, exchange rates are closely related to productivity because they are related to the purchasing power of the pound. If a significant volume of trade is based on higher quality lower priced British products and services, then pounds are required to purchase such goods and services. There is therefore a trade off between productivity and producer price-setting and this is something the BoE can do nothing about. On the other hand PPP not only encourages higher productivity it achieves this on the basis of price-setting as well as investment so the impact can be short, medium and long term. This stabilizes the purchasing power of the pound, as opposed to devaluing it, and therefore exchange rates do not have to fall to lower levels in order to gain exports or substitute exports. This is because the Real Incomes approach augments the real incomes of importers of British goods and services who pay using pounds. Germany has managed to achieve this, albeit through other means. The UK needs to move from conventional monetary and fiscal policies and focus on a Real Incomes policy that helps establish a more stable and even increasing exchange rates for pounds against foreign currencies.

Inflation and deflation

PPP has a positive control over inflation through the use of the price performance ratio (PPR) as the key determinant variable in the price performance levy (PPL). Inflation is completely controlled by advantageous unit price-setting by economic units, facilitated by the bonus payments that accrue with lower PPRs and, therefore, lower PPLs. Any deflation would be the result of conscious decisions by specific economic units attempting to maximize their incomes through market penetration on the basis of setting unit prices at lower levels. The fallacy of run-away deflation causing people to delay purchasing goods and services in the hope that they will fall further does not arise because the lower price bounds are set by technical and physical production constraints so unit price declines will naturally stop at the point at which real incomes of the economic unit cannot be raised through further unit price reductions. This presents an interesting consideration in the redesign of marginal pricing theory to take into account total revenues and real incomes as opposed to nominal profit margins.

1 Hector McNeill is the director of SEEL-Systems Engineering Economics Lab.

Updated 2nd July, 2015; Typos

Updated 3rd July, 2015; Elaboration for clarity - original sense maintained.

Updated 20th July, 2015; Added box, box text and diagram.

Updated 21st July, 2015; Altered diagram to clarify desirable directions of movement in variable values.

Updated 21st July, 2015; Added sections: "The significance of real incomes as a policy objective

" and "Growth in the economy".

Updated 24th July, 2015; Added missing text concerning the role of the PPR in the box.

Updated 24th July, 2015; Added additional explanation concerning exchange rates after hearing Mark Carney replying to a Parliamentary Committee question concerning exchange rates.

Updated 31st July, 2015; Changed expressions but sense maintained.

Updated 14th August, 2015; Added why and what sections (see new intro).

All content on this site is subject to Copyright

All Copyright is held by © Hector Wetherell McNeill (1975-2015) unless otherwise indicated

|

|

|

|