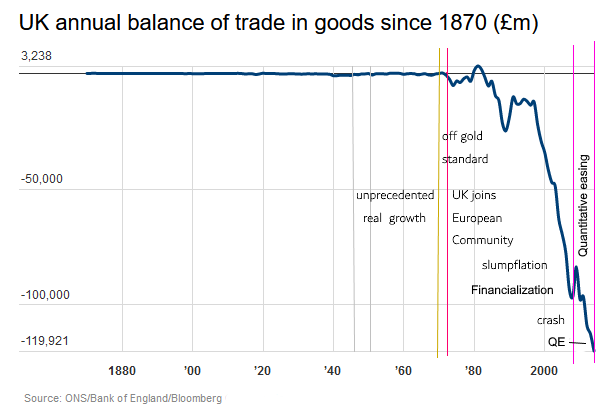

The hard data recorded in graphical form on the left maps out a story starting in 1945 with rising real economic growth, full employment, adequate investment and rising productivity and declining income disparity switching in 1970 into a decline in competitivity of goods produced in the United Kingdom. This resulted in the initiation of a decline in the balance of payments as a direct result of the adoption of monetarism in 1975 following the 1973 geostrategic decision of the Organization of Petroleum Exporting Countries (OPEC) to raise international petroleum prices seven-fold within a decade. The combination of the failure of the Gold Standard in 1971 and the recycling of petrodollars into selected petroleum importing countries, witnessed an explosion in financialization. This was facilitated by governments deregulating the financial sector in response to intense lobbying and a rush to globalization. This undermined industry and manufacturing in countries such as Britain.

Lesson One: In general out of control goods and service price inflation comes from rising input costsThe main outcome of the OPEC sanctions was a potent cost push inflation affecting most countries in the world most of whom relied on petroleum imports. The intensity of the inflation caused a failure of some operators to remain in business resulting in layoff and rising unemployment to create stagflation or slumpflation the combination of inflation with rising unemployment. Keynesianism offered no solutions to this predicament and monetarism even less so. However, the obvious inability of fiscal actions or government loans and expenditure to resolve this exogenous cost-push impact resulted in attention being given to monetary policy instruments as a possible solution. It was more than apparent that monetarism was as useless as Keynesianism in solving this serious problem.

Since government borrowing and expenditure and interest rates and debt offered no solution, it was very apparent that an alternative solution was required.

Lesson Two: Increasing financial debt is not a solutionRather than advocate this type of approach, the International Monetary Fund (IMF) under Managing Director Johan Witteveen, did nothing to encourage OPEC to stop raising prices but rather used petrodollars to provide loans to low income countries to continue to purchase petroleum at ever-increasing prices. In 1977, riding on the prize event of providing the UK with a loan to attempt to stabilize the balance of payments the IMF published a book, "

The Monetary Approach to the Balance of Payments". The prestige of the IMF resulted in virtually no questioning of the logic of the highly academic book and prepared the ground to the monetarist takeover of the macroeconomic policy dialogue. This paradigm was the blueprint for increased international debt

Lesson three: Don't confuse apparent coincidences in data associations with cause and effect; identify the mechanismsHowever, the evidence for the rising influence of monetarism was flimsy and based more on ideological and a series of assertions as opposed to a transparent model of the mechanisms of how monetarism could tackle stagflation. The doubts as to the efficacy of monetarism can be traced back to 1970 when in the Lloyd's Bank Review, Nicholas Kaldor published an article entitled, "

The new monetarism". In this article Nicholas Kaldor expressed the opinion that Milton Friedman's assertion that money volumes create demand which results in economic growth was wrong with the sequence of events being the wrong way round. Investment, leading to real growth came from the requirements of supply side manufacturers, or example, so the demand and resulting economic growth originated in the supply side and not from "money volumes, banks or monetary policy. The banks responded to demands associated with the natural growth in the supply side production sectors.

Above is the cover of a book published in 20141.

The somewhat confusing title reflects the black and white binary mentality of monetarists and faith in the dictum that economic growth (expansion) can only occur if the public sector is reduced in size (contraction). Part of the argument is that,

"... public services are a drain on the economy"

or, the more colourful,

"... the public sector is there for freeloaders."

These Friedmanesque assumptions, like his failure to understand the mechanisms that govern the relationship between money and prices, seemed to reflect a lack of intellectual curiosity to understand why the public sector might have an essential role in the economy or how it might be made to contribute to real national growth. The most convenient option was clearly to cancel the possibility of any such considerations and continue to promote an unjustified dogma.

An example of this dogma was George Osborne's imposition of an unnecessary "austerity" which ran down essential public services with the able assistance of the Bank of England's quantitative easing, a more extreme variant on a policy with no theoretical foundations.

It is true that public funds managed by governments are quite often wasted and with very low impacts on productivity, costs and real economic growth.

However, under a Real Incomes Policy all public services would be subject to the same incentives as the private sector, resulting in the combination of more-for-less productivity-based growth with counter-inflationary impacts. In this way, all sectors of the economy, private and public, would contribute to a positive systemic consistency in economic benefits.

1 Needham, D., & Hotson, A., "Expansionary Fiscal Contraction", Cambridge University Press, 2014. |

|

|

Friedman responded to Kaldor's valid observations in a disrespectful, off hand and dismissive fashion, stating that "

Professor Kaldor is a Johnny-come-lately"

In 1975 starting out on the work leading to the real incomes approach, I had noticed that Milton Friedman in appearances during the late 1970s, was never able to explain the specific mechanisms whereby money volumes cause inflation in the prices of goods and services. Whenever asked Friedman would become somewhat adamant and defensive and assertive. His default "explanation" was that "

..this happens in the long run!" , which, of course, is not a mechanism.

Robert Neild, in a section of the book "

Expansionary Fiscal Contraction" (see box on right) published in 2014. Neild refers to Friedman's assertion that inflation is the result of excessive expansion of the money supply and that by restricting supply, the economy, being self-regulating, would soon return to the 'natural rate of unemployment. However, Friedman never explained the cause and effect mechanisms involved. Robert Neild and Frank Hahn wrote a letter to the Times in 1980, criticising monetarism stating that with market imperfections, a reality, there were no specific elements to suggest the economy would return to some equilibrium point automatically as Friedman asserted.

For what it is worth, Nicholas Kaldor, some time before this, had explained that adding "equilibrium seeking" functions in econometric models did not square with reality. The economy is always in a disequilibrium and the more innovative the economy, the more change occurs to disturb any "equilibrium".

Friedman did not appreciate Neild and Hahn's letter and in a somewhat aggressive reply to the Times he included a choice statement,

"We can know that a bird flies and have some insight into how it is able to do so without having a complete understanding of the aerodynamic theory involved.".

This redundant statement and is just flippant and did not address the issue of importance for any serious economic policy designer of the need to understand the specific mechanisms involved in order to understand the likely effects. If this is not important, are we accepting that the default function of economists is to risk the wellbeing of the whole national constituency by exposing it to an unproven socio-economic experiment that has no theoretical foundations?

Friedman then listed in his reply, a series of points, to the effect that there was an historical association between money and prices, with variable time lags. Without offering any better causal explanation than that, he reasserted in remarkably strong terms his view that the economy would recover automatically from the monetary squeeze.

Later, in a live debate with Friedman, Neild has stated that he found Friedman's constant ability to avoid saying what caused the historical association between money and prices, by means of prevarication and mockery very annoying. However, this did expose the fact that Friedman did not in fact know what the mechanisms were, and frankly, did not seem to care.

In 1981, 362 additional economists signed a letter prepared by Hahn and Neild, to the Times, criticizing the Conservative goverment Budget combining supply side economics elements with monetarist elements.

The reality is that while making a valid criticism the authors did not make any alternative proposition. Indeed, Sir Geoffrey Howe, the Conservative Chancellor at the time, noted the lack of any proposition attached to this letter. It is unlikely that they had any alternative propositions because the then "alternative" Keynesian instruments could have no impact on cost-push inflation. The basis for a solution lay in the then past works and statements of Nicholas Kaldor linked to technology and innovation.

Lesson four: trying to engage with policy bubbles can be a waste of time, they are seldom receptive to changeIn 1981 I circulated a monograph on the Real Incomes Approach to all political parties to provide, at least, an optional policy. However, each remained in their own bubbles and appeared to be incapable of even contemplating the possibility of logical alternatives existing. The only MP to engage on this topic and who clearly understood the concepts, was Richard Wainright of the Liberal party economics spokesman.

Lesson five: The Quantity Theory of Money does not apply to goods and servicesIn reviewing the results of quantitative easing (QE) in 2020, and having worked on the analysis of inflation since 1975 it became very evident that the Quantity Theory of Money (QTM) was completely wrong. The identity is supposed to relate the volume of money to the prices of goods and services so with QE it would have been expected that the excessive volumes of money would result, according to the QTM, in excessive price inflation in the short run. This did not happen. There was indeed inflation in the short run but the prices affected were those of assets in markets which became speculative as a result of large volumes of money entering them. Goods and service prices remained relatively stable. Over time, it took about a decade, the prices of goods and services began to rise as a result of significant price rises in assets which were also input costs to supply side production of goods and service activities, causing cost push inflation. Obvious examples were land, domestic and commercial real estate and commodities subject to speculative hoarding (agricultural and energy commodities) which in turn impacted agricultural production costs and industrial and domestic costs in general.

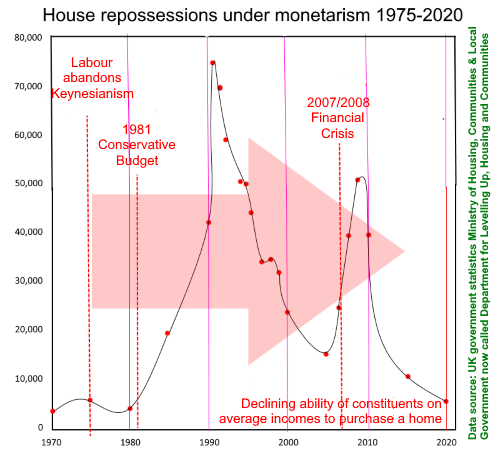

For many families, gaining the ownership of their home is an important quest. In the pre-1975 conditions constituents with average incomes could afford to purchase a house to suit their needs based on mortgages, usually through mutual building societies. The Conservative party championed home-ownership (see poster on right).

The thoughtless introduction of monetarism as the dominant macroeconomic paradigm led to the Thatcher government raising interest rates to tackle stagflation. There was no theoretical foundation for such a decision other than assertions of people like Milton Friedman.

As a result, what were totally sound mortgage agreements, taken out in good faith, were converted into sub-prime mortgages by an inappropriate policy, leading to thousands of families losing their homes through repossession. Even although this was the result of the imposition of a policy with no theoretical foundations and, therefore, no justification, the Conservative government never offered any form of compensation.

Beyond the boundaries of such irresponsibility the government's reliance of quantitative easing led to speculative price rises in housing and succeeded in placing house prices well beyond the reach of average income constituents. |

|

|

The QTM, in various formats, has been around for centuries and since it was the preserve of the elite it is logical to assume that its original purpose was to show the connection between money volumes and asset prices, the main and continuing interest of the elites. In these relationships the original QTM can, indeed, demonstrate a cause and effect relationship reasonably well. Somehow, as a result of the more evident concerns of the people of the country, in a period experiencing the rise in universal suffrage, being linked to the prices of goods and services, governments and monetarists assumed the QTM also applied to goods and services. Certainly the "modern version" created by Irving Fisher (1867-1947) and "applied" by monetarists, serves no such purpose at all. The prices of goods and services are established by the conditions of each competing company and not by money volumes in the economy.

This error continued to be a committed by monetarists because there seems to have been an assumption of the same cause and effect relationships without anyone bothering to enquire into the mechanisms involved. Monetarists, continued to insist on relationships which do not exist in reality and this is why, when challenged, they could never identify or explain the mechanisms involved.

Lesson six: Monetarism, in its current form, undermines constitutional principles of equality of treatment of the members of society This combination of ignorance and arrogance has meant monetarism has remained the principle force in macroeconomic policy and, being an elitist interest, has resulted in the main policy benefits flowing to a wealthy elite making up something like 5% of the national constituency, a state of affairs made very evident under QE. The damage created by this approach to economics is summarized in the recent BSR Note,

"The constitutional crisis created by monetary policy".

Lesson seven: Nothing in economics is that complicated; nothing is inevitable if people are prepared to contemplate what is happeningBy simply rearranging the components of assets, goods, services, saving and offshore investment in a Real Money Theory identity, I was able to create a more comprehensive version of the Quantity Theory of Money, and which provides a map of where money flows and impacts prices, an analysis that is impossible with the QTM. It is not as if this was a complicated bit of work, it was not. However, with so much apparent intellectual effort having established a legacy of economic theory and policies, the failure to focus on why things go wrong is lamentable. This sort of analysis cannot be undertaken by rhetoric and counter assertions or by politicians thinking on their feet and trying to attract votes. It can only be resolved by standing outside this capsule which is heavily bogged down by ideological baggage and to conduct a dispassionate and objective systems engineering economics review of cause and effect mechanisms and to review how these can be managed to effect a more balanced support for constituents' needs.

Lesson eight: Identify common interests to gain a coherent support through public choice on policies to be pursuedAt the moment economic policies are extremely biased towards the interests of a small group of constituents. Therefore, in this analysis it is important to take into account what one would consider to be a more generally applicable voter decision preference. To be clear, this means identifying objectives with which all can agree and offer their support. In the quest to identify such a commonly supported objective my own work identified real incomes as the most significant likely common interest of all. Nothing has appeared in economic theory or in practice to cause me to doubt this fundamental policy target and the most important policy objective. What is very evident is that no conventional policies can support this objective because of the inherent bias in policies which have no theory or historic evidence to justify them.

Lesson nine: Beware of over-confident assertive "experts" who wish to apply solutions that have no theoryIn argument, Friedman was assertive and combative. This is exactly the sort of behaviour that impressed and helped convince less well-informed politicians to believe that his apparent confidence reflected a deep understanding of matters beyond their understanding. The reality is that this was clearly not true. They faced an effective one-man propaganda machine managed by a man who had a poor grasp of the critical mechanisms of the very subject he was lauded to be the leading "expert".

This country, through the Bank of England and, indeed, the world through the International Monetary Fund and central banks, have paid a heavy price as a result of a non-critical acceptance and application of the policies he advocated.

1 Hector McNeill is director of SEEL-Systems Engineering Economics Lab

Hahn, F., & Neild, R., "Monetarism: Why Mrs Thatcher should beware", The Times, 25 February, 1980. & Friedman, M., "Monetarism: a reply to the critics", The Times, 3 March 1980. McNeill, H. W.,"A Real Money Theory", DIO, 2020 and various subsequent elaborations in the series, "Charter House Essays in Political Economy" 2021 and 2022, Lord Kaldor, "The Economic Consequences of Mrs. Thatcher" in Butler, N., "Speeches in the House of Lords 1979-1982", Duckworth, 1983. Kaldor,N., "The new monetarism", Lloyds Bank Review, 1970; Friedman, M., "The New Monetarism: Comment", Lloyds Bank Review,1970.

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2022) unless otherwise indicated