This article is an interview with Hector McNeill a British economist who, in 1975, initiated the development of the Real Incomes approach to economics an alternative approach to macroeconomics. His motivation was to investigate why Keynesianism and monetarism, and subsequently supply side economics (KMS policies) were incapable of avoiding serious and arbitrary prejudice on the economic and social constituencies resulting from commodity price or financial shocks and why policies designed to resolve the economic crises further exacerbated the prejudice in an arbitrary manner.

The Real Incomes Approach to economics has evolved, over the years into a distinct macroeconomic and microeconomic theory accompanied by a set of decision analysis options embodied in sets of coherent

This approach is designed to avoid most of the disadvantages of conventional policy practice.

However, McNeill remained dissatisfied with the fact that there were some issues which appeared to be defy resolution centred on what he refers to as the "profit paradox". In October 2014 McNeill came across an article by Peter Drucker that referred to Joseph Schumpeter's view on the role of profits which, according to McNeill, represents an important contribution to the solution of the "profit paradox". McNeill considers Schumpeter's contribution to provide an important clarification of most of the outstanding issues facing macroeconomic policies. These have a significant impact on microeconomic theory as well as providing a basis for a more efficient and optimized operation of fiscal policy. As a result McNeill embarked on a full revision of the theory and policy implications of the Real Incomes Approach in November, 2014. He considers the current evolving version to provide a more transparent analysis and basis for resolving today's main macroeconomic policy challenges.

What follows is a summary of the second interview given by Hector McNeill since this realization and entitled:

, where he explains how the "missing link" in the form of the solution to the "profit paradox" based on the Schumpeterian perspective provides a key to unlocking outstanding and unresolved issues in the theory and practice of the Real Incomes Approach. The first interview entitled

, reviews the overall problems with conventional macroeconomic theory and policy centering on the "profit paradox".

These interviews took place in Portsmouth, Hampshire, England during November, December, 2014 and January 2015. An additional interview was completed in late February early March 2015 covering Hector McNeill's views on the political changes affecting Greece and the EuroZone, this interview is entitled:

In order to facilitate reading I have added subtitles to this report. The Real Incomes approach has introduced a range of new concepts to economics, some of these are somewhat technical. Where these are mentioned I have provided references to sources for those interested in exploring these aspects in more detail.

Macroeconomics, a solution

Nevit Turk: In our chat, before this interview, you mentioned what you consider to be an important observation made by Peter Drucker on Joseph Schumpeter's views concerning profits. Is this an appropriate point to review the significance of this?

Hector McNeill: Yes it is. The confusion over profits caused by its contradictory roles exacerbated by an inappropriate accountancy framework and target for taxation is caused by an even more bizarre norm of people assuming the economy runs on the basis of aggregate demand and the profit motive. And yet we can easily appreciate that profit is a very poor objective and indicator of economic performance. The result has been that so-called "demand" and the "profit motive" has resulted in microeconomic management decision-making being subject to policy-induced constraints

3 that impose a tendency to misallocate resources at the level of the firm and, by extension, the macroeconomy. Therefore economic activities will have lower productivity than the potential. This is what has led to the general systemic prejudice that we observe suffered by segments of the social and economic constituencies.

Joseph Schumpeter on profit

Joseph Schumpeter made an important observation that the significance of profit is that it is the guarantee of future activities (through investment) and of future employment (through a rational choice of technologies). This has been cited by Peter Drucker in a paper published in Forbes in 1983 ( see

Schumpeter and Keynes ). If this became the exclusive purpose of profits then the Marxist analysis concerning excess production would have no basis in fact. This rationale supports what I have called the profit paradox

4 in that this aspect of Schumpeter's view is at odds with current concepts of the role of profit. The concept of profit is poorly defined and its role devisive in terms of the operational efficiency and transparency of the economy. In my opinion, limiting the role of profit to the aspects expressed by Schumpeter's observation is entirely valid and it opens a doorway to the resolution of this confused resource allocation issue that circulates around profit. This is achieved by substituting the quest for profits by a quest for real incomes.

Increasing real incomes by facilitating allocative optimization and higher productivityCorporate founders, shareholders, senior management and wage earners are all involved in the activities of an economic unit to earn income. If accountancy norms were changed to substitute profits by real incomes as the single corporate objective and a single accountancy variable the allocative efficiency and effectiveness could be significantly improved leading to higher productivity.

Nevit Turk: Are you saying profits no longer have a rational function and that accountancy norms therefore have to change? If so, what would be involved here?

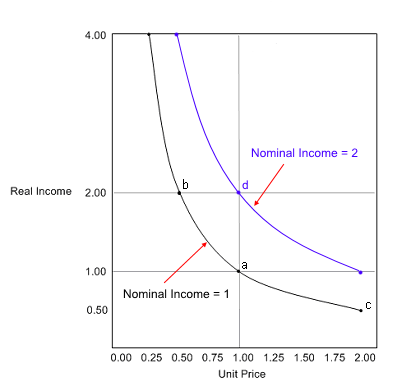

Nominal Incomes, Unit Prices & Real Incomes The measurement of real incomes is more precisely determined with respect to the circumstances of any particular individual.

Thus one can measure real income in terms of individual nominal income (iNI) and the prices paid by that individual as individual average unit prices (iAUNP) as a basis to provide an individual real income level (iRI).

Thus iRI = iNI/iAUNP ........... (1)

Where

iRi is an individual's real income;

iNi is an individual's nominal income (disposable)

and iAUINP is the average unit prices paid by that individual.

If the iNI is fixed in the short term at say 1.00 (see graph below) and one takes a starting position where the average unit nominal price is 1.00 then the instantaneous real income associated with these two variables is also 1.00. See point a in the graph.

A halving of unit average nominal prices to 0.5 increases the individual real income level to 2, as depicted by point b in the graph.

Lastly, as individual average unit nominal prices rise, in the short term, real incomes fall. For example, a doubling of the individual average unit nominal prices ends up with the individual real income level falling to 0.5 as shown by point c in the graph.

Rising nominal incomes do not necessarily result in higher real incomes. Thus the real income effect of unit prices shows that the real income of someone with a nominal income of 1.00 but paying an average price of 0.5 is the same as someone with a nominal income of 2.00 but who is paying an average price of 1.00 - compare points b and d.

Note that the item iRI can be equated to the quantity of goods, services and money purchased by an individual i.e. iQgsm, thus:

iQgsm ~ iRI = iNI/iAUNP .................. (2)

Thus real income appears to be equivalent to the purchasing power of income expressed as the quantities of desired goods, services and money which can be purchased for a given nominal income.

|

|

|

Eliminating taxation from business allocative decisions

Hector McNeill: If real incomes became the macroeconomic and microeconomic objective, the increased coherence between business and social objectives can result in higher levels of economic performance (productivity) and increased real incomes. To deliver on this promise, policy needs to provide positive and practical incentives for actions to increase productivity and the attainment of sustained or growing real incomes. The policy instruments deployed need to be able to influence the essential components making up real incomes including productivity, unit output prices, the value of the currency and income distribution.

Given the perverse incentives and contradictory motivations surrounding profits it is clear that it is difficult for economic units to optimism their resource allocation, efficiency and therefore the full potential productivity cannot be fully realized. Rather than confuse the allocative rationale by including tax, it is preferable to remove considerations of taxation and to first of all maximize the incomes of corporate founders, shareholders and employees according to productivity and their contribution to the operation of an economic unit. Once this is achieved through enhanced productivity, consideration of the amount of contribution that is made to government revenue can be more appropriately, transparently and precisely undertaken. The accountancy and audit framework can accommodate this change which involves conventional profit being substituted by real incomes.

Nevit Turk: Can you identify the steps of the transition required in policy? How would this work?

Real Incomes

Hector McNeill: First of all, we know that for a given nominal sum of money, the purchasing power of that sum depends upon unit prices and unit prices depend on the productivity of the economic unit producing goods and or services. The lower unit prices are, the greater amount of goods and services that given monetary sum can purchase. Thus a given nominal disposable income can purchase more with lower unit prices so that the real disposable incomes rise according to the degree that unit prices decline. ( Note, see box on the right. NT )

Productivity & prices

In order to take advantage of these relationships policy needs to provide incentives to encourage a tendency for economic units to increase productivity and to reflect this productivity increase in stable or falling unit prices. There is, of course, a trade-off between unit prices and product or service quality, but better quality tends to become the norm with marginal cost consequences in an efficient production or service system. This can be used to enhance real incomes if attention is given to the defence of the value of the currency. Unfortunately conventional policies tend to ignore the relationship between productivity and currency value and make currency value a resultant of monetary policy based on monopolistic centralized state interventions involving arbitrary interest rate-setting, money supply and bonds, as opposed to the real productivity of the economy. Thus the overwhelming force in determining monetary value is policy as opposed to the productivity of the economy.

Nevit Turk: But the purpose of monetary policy is usually framed in terms of securing price stability to maintain the value of the currency.

Monetary depreciationHector McNeill: Monetary policies based on interest rate-setting and money volumes contribute to a depreciation of the currency (especially low interest rates and quantitative easing) because a 2% inflation is considered to be a target whereas a 2% inflation results in a real incomes depreciation because of the fall in the value of the currency by roughly 18% each decade. I should add that this does not take into account the rise in the size of the population which further stretches output over larger population further reducing real incomes.

The Price Performance Ratio

A sound policy should promote productivity rises which for consumers and purchasers of capital equipment and services is manifested by moderated or falling unit prices resulting in rising purchasing power and real incomes. The performance of economic units in increasing productivity can be measured by their price performance ratio (PPR).

Nevit Turk: I'm not sure I have heard this term price performance ratio, what is that exactly?

The Price Performance Ratio (PPR)

A more detailed explanation of the Price Performance Ratio can be found here: NT

Source: McNeill, H. W., Solving the PPR Puzzle Real Incomes Org., 2013.

|

|

|

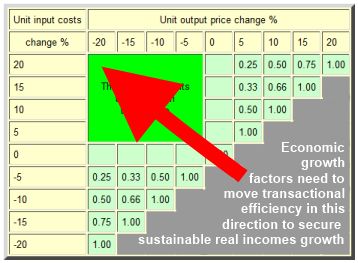

Hector McNeill: The price performance ratio or PPR is a central performance measure within the Real Incomes Approach that I introduced in 1976 to facilitate the analysis of the dynamics of price changes and their impact on real incomes. It is a measure of the dynamic response of output unit prices to changes in unit input costs. So if unit costs rise by 10% and unit prices rise by 5% one ends up with the economic unit "absorbing" inflation and attaining a PPR of 0.5 (less than unity). In general terms companies with PPRs greater than unity (1.00) increase inflation and those with PPRs of less than one, decrease inflation.

However, the achievement of low PPRs by any particular company at any particular time depends upon the input and output market conditions, the potential levels of physical productivity offered by state of the art technologies and the levels of capability or skills in the management of optimized techniques on the part of the human resources employed. Depending upon company size, cash flow status, and access to resources, the range of feasible PPRs depends upon technical determinants or feasible input-output ratios, upon knowledge of the main determinants of productivity, and upon the likelihood of achieving best practice with current technological and human resources. Even although a company management might not have adequate knowledge and information to take performance targeting decisions, the mapping out of PPRs can help identify the potential productivity leading to the identification of ways to allocate technological and human resources to improve performance.

Why PPR? Nevit Turk: Why can't normal inflation indices be used?

Hector McNeill: The PPR is estimated at the level of the firm and is not a general index (although by aggregating PPRs a general index can be generated) and it measures changes in unit prices directly. Unit price is the only expression of exchange equivalence. Quality variations and elasticities of substitution related to new products and changes in relative or changes in qualities are difficult to accommodate in common indices. In reality, the �baskets� of relevant commodities, goods and services, that might be used to determine an index, vary with each person or economic unit according to the time period of observation within a series of over-riding cycles that are specific to each person or economic unit. The PPR reflects unit price movements from the standpoint of productivity as opposed to purchasing power of some fixed nominal income. Clearly PPRs lower than unity (1.00) signify the probability that consumer real incomes, or purchasing power, will rise as a result of differentials between unit input costs and unit output prices and PPRs greater than unity signify an inflationary trend and a situation of lower purchasing power and real incomes on the part of consumers.

The real change in real incomes depends upon the degree to which gains in real incomes or purchasing power of consumers and capital purchasers is compensated by gains in real incomes of the owners and employees of the economic units producing or providing the given goods and services. The need to accommodate the conflicting demands of the profit paradox separates any positive incentive to trade-off purchaser gains against corporate ownership and employees. This leads to a concentration of income in the corporate ownership group and a decline in relative income for employees, as a group. It also is associated with a lack of a general incentive to pursue a competitive pricing strategy. A competitive pricing strategy is characterized by a general attempt by economic units to gain market share in increase returns to investment expressed as income by exercising a proactive price-setting approach. Proactive price-setting involves the establishment of unit prices designed to gain market share and, in the case of a real incomes policy, to lower unit prices. This is hampered by the current conflicting priorities imposed by conventional policies that fail to resolve the profit paradox.

Nevit Turk: Can you explain how PPR values help companies in their decision-making?

PPR MapsHector McNeill: The viable PPR maps vary for each type of economic activity, the factor and product markets, the technologies deployed and experience of personnel.

A PPR Map

Each company will be operating at specific locations within this mapSee

McNeill, H. W., Solving the PPR Puzzle Real Incomes Org., 2013. for detailed explanation

Price Performance Ratios (PPRs)

associated with different unit input value movements & movements in unit output prices

| Unit input costs | Unit output price change % |

| change % | -20 | -15 | -10 | -5 | 0 | 5 | 10 | 15 | 20 |

| 20 |

This area represents

the innovation

target zone | 0.00 | 0.25 | 0.50 | 0.75 | 1.00 |

| 15 | 0.00 |

0.33 | 0.66 | 1.00 | |

| 10 | 0.00 | 0.50 | 1.00 | | |

| 5 | 0.00 |

1.00 | | | |

| 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | | | | |

| -5 | 0.25 | 0.33 | 0.50 | 1.00 | | | | | |

| -10 | 0.50 | 0.66 | 1.00 | | | | | | |

| -15 | 0.75 | 1.00 | | | | | | | |

| -20 | 1.00 | | | | | | | | |

Innovation target zone | | Desirable states | | Undesirable states | |

|

PPR Maps can be aggregated so as to identify sector innovative target zones so that they can be used by corporate managers to identify optimized competitive growth strategies and tactics. The real ability to move a company's operations towards an innovation target zone so as to become increasingly competitive depends upon an assessment of the trade-off between investments in technology and human resources in response to changes in input costs (made up of fixed overheads as well as variable inputs). Depending upon the state of factor and product and service markets, the achievement of higher productivity and margins depends upon a proactive reconfiguration of the key input factors.

Direction of travel to secure increasing performance and real incomes

The ability to identify critical resource allocations enables a more rational discussion of common interests between companies as well as sector and the government policy-making areas. This does not imply any loss of competitive or strategic information since information can be divided into clear information categories including: (1) the current state of the art of relevant technologies, (2) the range of operational practice achieved associated with variations in applied human techniques, (3) the needs of the members of an economic sector used to promote common interests related to policy, (4) the contribution of a sector to the economy and social constituency used to promote pubic image of sector and development and (5) innovative knowledge and information unique to each company and not shared between companies.

One of the benefit arising from a more detailed analysis of corporate processes involving technology and human resources is that it is often possible to identify ways and means to improve productivity significantly on the basis of better operational management and in particular taking care to ensure that people are provided with adequate circumstances to learn from repetitive processes so as to descend the learning curve and achieve higher levels of competence and productivity. In a prototype decision support model I produced in 1988

5 it became evident that significant gains in productivity could be obtained without large investments and prolonged investment cycles.

Nevit Turk: Can you relate this aspect of decision-making to the profit paradox?

Solving the profit paradox

Currently there is an emphasis on the accounting variable profit. Companies that maintain or lower unit prices in the face of rising unit costs end up with lower profits. The perversity of three conflicting allocative constraints related to profit maximization, taxation minimization and wages constraint compromises resource allocation procedures so as to end up with suboptimal allocations. In order to eliminate the current system's source of inefficiency and uncompetitive pricing, profit, as an accounting variable, needs to be eliminated. In addition, by also removing tax considerations and profits from allocative decisions by substituting profits by investment in technology and human resources corporate resource allocation can be transformed into a more efficient and effective model to secure growth in real incomes benefiting firms, people and the economy in general on a sustained basis.

The necessary process involves some simple transformations in accountancy details. Thus, if we eliminate corporate taxation from the decision analysis model, we are left with five basic categories of quantifiable aggregates:

- Corporate revenue from sales

- Income of individuals associated with the company

- Savings and saleable assets

- Profit

- Current operational costs

|

As mentioned, the profit category can be redefined as investments in technology and people. So the accounting categories can be expanded to six:

- Corporate revenue from sales

- Income of individuals associated with the company

- Savings and saleable assets

- Investment - technology

- Investment - human resources

- Current operational costs

|

Increased productivity can be reflected in lower unit output prices being associated with lower Price Performance Ratios (PPRs). However the manipulation of PPRs needs to remain in the hands of corporate management so as to adjust values according to the ability of the company to optimize resource allocation to maximize income.

Virtual red tape imposes constraints and reduces business options and efficiencyThere is a need to eliminate the virtual red tape made up of policy-imposed constraints relating to taxation, profit maximization and wage control that severely limit the options open to business to raise productivity through efficient forms of resources allocation. The broad strategy needs to be to remove constraints and increase the range of options open to business.

The need to support effective business rules to secure efficiencyUnder conventional policies, there is a lack of coherent business rules that effectively link up microeconomic imperatives with overall macroeconomic objectives. With this new accountancy structure it is easier to align macroeconomic and microeconomic objectives.

Nevit Turk: How can the Real Incomes Approach help provide the appropriate support for this alignment?

Price Performance PolicyHector McNeill: One option for applying a Real Incomes Policy is Price Performance Policy (PPP) which provides a sustained positive incentive for companies to invest to raise productivity. It does this by lowering the risk associated with actions designed to reduce unit prices. This is achieved by applying a Price Performance Levy to the operational margin. The levy varies in value according to the inverse of the PPR achieved by a company. The lower the PPR the more competitive unit output prices have become with a direct impact on real incomes of consumers. In compensation the PPL is lower than in the case of companies maintaining a higher PPR indicating a less responsive reaction to inflationary input prices. However, the Price Performance Levy is only a productivity incentive. It is not a fiscal instrument or a means of generating government revenue. Also it is not a subsidy, any transaction only involves money generated by the firm's own activities.

The PPL couldn't be used as a reliable source of revenue in any case since as the economic performance of firms rises the amount raised would decline sharply.

Nevit Turk: How can a manager control the value of a firm's PPR to ensure a lower Levy?

Corporate Margins as the PPL target

Hector McNeill: The margin of the company is corporate revenue reduced by deductions including: (1) owner, shareholder and personnel incomes, (2)additions to corporate savings & acquired assets, (3) investments in technology and human resources and (4) current operational costs. A manager therefore has a very large range of allocative resources being able to marginally adjust total unit input costs upwards or downwards. Thus unit output price reactions are not only measured in terms of unit variable input cost variations. In this way the management has a more effective control over costs. Having eliminated profits from the allocative logic there is no longer any profit paradox conflict between shareholder income, taxation minimization or employee wages.

Fortunately the full range of methods for microeconomic optimization logic remain fully applicable and indeed, are more effective. These include a large range of proven optimization methods including marginal costs pricing, linear programming and the Monte Carlo method. A significant advantage is that decision-makers are not limited to working with established market prices but can also review and simulate more appropriate unit prices so as to lower their PPR and gain higher per unit of output margins while reducing unit prices and gaining market penetration through increase quantity of sales (units of product or service). Therefore marginal cost pricing is not constrained by operating within an environment of passive price-taking but in one of innovative proactive price-setting.

Managers can manage corporate affairs so as to attain PPRs that ensure the highest revenue for their company. Naturally, how they do this, depends upon the individual circumstances of their economic units and the markets they sell in to. Therefore managers need to become more market responsive and attentive to market conditions and reacting by applying business rules that permit them to manage and determine the headline PPR for their company so as to maximize revenue.

Management decision-making and judgement concerning risk still remain in play since a too aggressive unit price reduction might not gain the consumption response and market penetration desired leading to lower than expected corporate revenues. On the other hand government has no role whatsoever in this decision-making whereas companies establish their own PPRs. In this way the business rules are coherent with the macroeconomic objective of attaining higher real incomes through an allocative process that is both a counter-inflationary and real incomes-enhancing.

Nevit Turk: How would the incentive provided by the Price Performance Levy operate?

Hector McNeill: The Price performance Levy (PPL) is a levy whose value is determined by a company's Price Performance Ratio (PPR) thus the PPR is the main variable in the PPL equation and it is used to weight the size of the levy paid. There is a large range of possible formulae for the PPL. These can designed to reduce, augment or intensify the influence of the PPR on a PPL and therefore the resulting corporate margin. For example, in order to intensify the incentive for companies to secure a low PPR value, use can be made of a PPL formula that makes use of a power function where the PPR is raised to some power such as being squared. For example such a PPL formula would be something like: PPL = L.(PPR

2). Where L is a fixed value basic levy of say 20% so that with a PPL associated with a range of PPRs would be, for example, 0% for a PPR of 0.00 equivalent or a rebate of 100% or 11.25% for a PPR of 0.75 equivalent to a rebate of 43% to 20% for a PPR of unity (1.00) equivalent to a rebate of 0%, that is the payment of the full Levy of 20%.

Nevit Turk: You stated that the PPL is not a fiscal policy or means of raising government revenue. How would governments raise revenue to pay for public services?

Hector McNeill: The solving of the profit paradox means that there would be no profit category and no corporate taxation. But all government revenue would be raised from incomes. Thus income taxes would be paid by corporate owners, shareholders and employees. Those companies securing low PPRs would benefit from higher per unit of output margins and in particular rebates can be paid as income bonuses so as to compensate all associated with a higher productivity company with higher gross incomes. Value Added Tax (VAT) can be used to make up shortfalls in revenue raised from personal incomes.

Nevit Turk: How would the income payments work since from what you have stated it appears to mean that incomes will vary?

Hector McNeill: All incomes should be related to reasonable pay scales. Owners and shareholders could have a fixed income estimated on the basis of capital contributions or holdings and employees would have a professional pay scale related to function, qualifications and experience. Bonuses would be paid over and above these fixed incomes in relation to the group performance and the PPL rebate achieved.

Nevit Turk: What about low paid workers? How can they pay tax and contribute to revenue?

Hector McNeill: Good point. Well the basic pay scale should be a living wage enabling each individual to cover basic essentials plus an additional amount that is nominally destined for tax. The whole notion of a significant proportion of the workforce not being able to pay tax is a reflection on the decadent nature of productivity in our economy. Price Performance Policy is designed to assist the economy move in a direction that enables people to contribute to revenue based on a sound human resources policy geared towards increasing economic performance or productivity.

The recent removal of a significant proportion of the workforce from any obligation to pay tax is a sign of failure and not of success; it means fewer people gain enough to be able to afford tax payments.

Nevit Turk: Is it possible to sustain this sort of growth in real incomes?

Sustained productivity and real incomes growth

Hector McNeill: Increases in productivity arise from technological innovation and the advance in technique based upon the accumulation of experience-based learning by individuals (tacit knowledge), learning from past performance in the form of gaining knowledge on the best components to use or the optimal physical machine settings in relation to efficiency and quantitative relationships between inputs and outputs (explicit knowledge). Therefore as part of the changes in unit costs used to calculate the PPR, it becomes more effective if investments in technology and human resources be introduced as costs so that the PPR can be lowered so as to pay a lower PPL. This has the effect of encouraging management to explore ways and means to improve price performance through careful incremental investments in technology and people.

In the Schumpeterian sense the price performance incentive encourages managers to invest in technology and people as the guarantee of future activities and sustained income. This guarantee is further bolstered by the fact that growth is based on productivity increases associated with a general rise in purchasing power and higher real incomes of those associated with a firm as well as their customers.

Nevit Turk: This would involve a significant change in thinking and actions surrounding policy making because of the fundamental difference in the theory supporting the Real Incomes Approach.

Hector McNeill: Well yes. Amongst the British political groups who reviewed an early brief on this policy proposal, Richard Wainwright, the Liberal Party Finance Spokesman, seemed to be the only person to have a good grasp of the business and employment implications. In 1981 he told me that the problem with the policy was that if it became part of their manifesto, and they won the election, they would be faced with the problem of implementing it! Fortunately it would not be that complicated since companies could opt in or out of such a policy. Obvious candidates are the energy companies. I should emphasis that those opting in would perform better and earn more that those opting out so the advance and acceptance of the policy would rely on the outcome to a fairly low risk transition policy.

Nevit Turk: Does this mean that in the end privatization of public services might, after all, become a way to reduce public service costs?

Hector McNeill: Paradoxically the answer is no. All that is required is for public service provisions to be subject to the same Price Performance Policy conditions as the private sector. This would provide a strong incentive for their performance to improve based on public service incomes being determined on the merit measured by improved productivity. This would change how budgetary provisions are made by government with allocations becoming more related to the changing unit price frontier and the evolution in productivity within each public sector activity.

It is very important to appreciate the fact that by removing the accounting category of profits, companies and any other organization, become more price competitive and contribute to real incomes growth at the level of the macroeconomy. The significance can be appreciated in the current comparison between mutuals, such as building societies and profit-making banks whose need to satisfy shareholder value makes them less competitive. Under a Real Incomes Policy all types of economic unit become more price competitive and can attain a better operational performance.

1 Nevit Turk is the economics correspondent for APE-Agence Presse Européenne.

2 coherent in the sense of being transparently linked and consistent in both macroeconomic and microeconomic activities seeking to sustain or increase real incomes.

3 Constrainted optimization procedures arise from the profit paradox described in the first interview in this series; For more details see the previous interview,

"Macroeconomics - the problems" and see item

4 below.

4 Profit Paradox - the profit paradox arises from the accountancy and audit legal framework in the UK that attributes of conflicting functions for profit. Profit is the accountancy variable that is subject to corporation tax, it is the measure of business success as well as being the maximization objective in resource allocation procedures which face the need to contain or lower wages to achieve that maximization objective. Thus the profit paradox is the existence of three conflicting attributes of profit that relate to the desire to minimize taxation, maximize profits and contain or reduce wages.The outcome is a lower than potential optimized solution to resources allocation. For more details see the previous interview,

"Macroeconomics - the problems"

5 Seel-Telesis was a computer program serving as a decision support in business resources allocation designed and implemented in 1988 and undergoing various versions through 1990. One important demonstration was that significant gains in productivity could be obtained through the careful re-design and layout of processes involving machines and people which did not involve major investment but represented low cost growth pathways. This work was supported by the Department of Employment of the UK Government through the Manpower Services Commission, Sheffield.