⊚

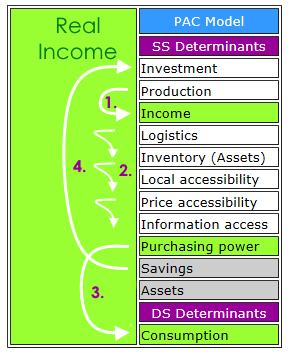

3. Purchasing power or disposable real income can be divided into savings, asset holdings or consumption

⊚

4. Some savings can be routed back through loans to investment

Important observations

- In link 2. supply side cash flow and availability for consumption will fall by the amount of product placed in inventory as a reserve of assets for future sale

- In link 3. the quantity of funds flowing into consumption and investment for production will decline if purchasing power (disposable income) is used for medium to long terms savings or asset purchases

Therefore falls in consumption can arise from unit price rises (inflation) that depress purchasing power of nominal incomes, accumulation of supply chain inventories as assets (hoarding) limiting supply, rises in savings (removed from consumption cash flow) and rises in asset holdings (removed from savings cash flow). Recent experience under Quantitative Easing (QE) has lowered interest rate to close to zero but increased exogenous money supply as low interest debt has been fed into assets resulting in a reduction in the volume of additional exogenous cash flow entering the transactional supply side activities.

The relevant Quantity Theory of Money that explains this distortion is the Cambridge Equation modified and nominated as "

Real Money Theory" (RMT) is shown below

M = (a + k) + (P. Y) ..... (iv) Where:

M is the quantity of money; P is the price level; Y real income. a is assets; and k is savings.

By bringing a and k to the left hand side as the divisor of M the strong depressive impact of rising asset holdings on the availability of money so as to reduce P.Y is evident:

| M - (a+k) = (P . Y) ..... (v) |

This explains how the exogenous funds that were not generated by the supply side have intruded so as to deny the supply side of funds for investment while channeling the exogenous funds into assets that would normally remain within the purchasing power of the supply side. However rather than see economic growth, in spite of close to zero interest rates, this has resulted in lower real incomes, lower substanative investment and deficient growth in productivity. As is self-evident, the rise in exogenous money did not have any practical impact on "aggregate demand"."

Without this intervention, incentives applied to the logistics elements of accessibility to products, information and unit prices facilitated a real income policy making use of the price performance ratio and price performance levey would have guided investment towards higher productivity and based on the endogenous supply side money cash flow achieve real growth in real consumption. This explains the basis operation of the Real Aggregate Growth Model (RAGM).

1 Hector McNeill is the Director of SEEL-Systems Engineering Economics Lab.

Updated to correct information on Real Money Theory - 30 July,2020.

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2020) unless otherwise indicated