Disjointed means no leverage

Part 1

Hector McNeill1

SEEL

Building back better is a hope expressed by many. A mix of booklets and books serve to illustrate why the UK has difficulties not only in perceiving what is needed but also lacking the popular agency to bring about necessary change. The booklet "Britannia Unchained - Global Lessons for Growth and Prosperity" (2012) and the books, "The Dignity of Labour" (2021) and "Greater - Britain after the Storm" (2021) were all written by MPs. "Britannia Unchained" of uncertain authorship carries the names of Kwasi Kwarteng, Priti Patel, Dominic Raab, Chris Skidmore and Elizabeth Truss all of the Conservative party. "The Dignity of Labour" is by Jon Cruddas a Labour MP and "Greater" is jointly authored by Penny Mordaunt of the Conservative party and Chris Lewis about whom there is little information. Building back better is a hope expressed by many. A mix of booklets and books serve to illustrate why the UK has difficulties not only in perceiving what is needed but also lacking the popular agency to bring about necessary change. The booklet "Britannia Unchained - Global Lessons for Growth and Prosperity" (2012) and the books, "The Dignity of Labour" (2021) and "Greater - Britain after the Storm" (2021) were all written by MPs. "Britannia Unchained" of uncertain authorship carries the names of Kwasi Kwarteng, Priti Patel, Dominic Raab, Chris Skidmore and Elizabeth Truss all of the Conservative party. "The Dignity of Labour" is by Jon Cruddas a Labour MP and "Greater" is jointly authored by Penny Mordaunt of the Conservative party and Chris Lewis about whom there is little information.

Britain faces major structural constraints affecting it's ability to recover in a globalized world. None of these documents pay sufficient any attention to these except in passing. As a result, three disjointed models are presented but are separated from the main driving forces creating Britain's plight and prospects for future recovery.

Given the state of academic economic theory and their derived policies, Cruddas has the sense not to propose any policies. However in the second half of his work he points out a crucial issue, the loss of vocation within the "working class" in the sense of professional competence, enthusiasm and pride in their occupation. This encapsulates much of which the other publications missed.

"Britannia Unchained" is more policy oriented in a disjointed sense of peering over the fence to see what other countries are doing and exclaiming, "We can do that!" "Greater" has a bit of that too, but is more reflective of the UK's relative dimensional context in the world and tries to justify confidence in the future by placing faith in the mix of traits and values of the population. "Greater" points out some of the drawbacks associated with Governance in the hope political parties might respond; they wont. This first part ona 3 part series explains in part why.

|

Hegemon: a leader, country, or group that is very strong and powerful and therefore able to control others: |

|

|

Some things are missingThe problem with all of these documents is they do not answer the question of

how to recover on an economic and politically practical basis combining mechanisms, procedures and policies. We explain below why this is the case. Clearly any level of hope in the "

Britannia Unchained" document, published in 2012 have been dashed by the failure of quantitative easing (QE) in the intervening 9 years (2012-2021) that hollowed out the economy and brought the country to a low point just before Covid-19 appeared.

The objective here is not to depress our readership, but rather to point out some realities which can help identify practical changes to bring about solutions to our current predicament.

Britain is caught in a trap shaped by historic events which repeat themselves. However, the cycles are multigenerational so the current generations no longer have the accumulated experience within their lifetimes to prevent the condemnation of repeating the same mistakes.

Hegemonic cycles The overall global context of current events is best understood from the standpoint of hegemonic cycles. All such cycles involved globalization, although we think this is a recent phenomenon. At the end of the globalization periods, hegemonic cycles end up with excessive capital accumulation, or money, resulting in the growth of financial speculation and a rising income disparity in the "home nation" or hegemon. This is our current state of affairs.

Known Universes

One of the important concepts identified by Locational-State Theory1 is the notion of the known universe of the constituency and leadership. This refers to the location of populations within hegemonic cycles and their priorities for actions responding to the dominant current stage in that cycle. As a result, what becomes the dominant scientific and technological capability and economic theory and practice is influenced by exposure to and need to respond to conditions associated with the hegemonic phase This impacts the thinking of all the then current generations.

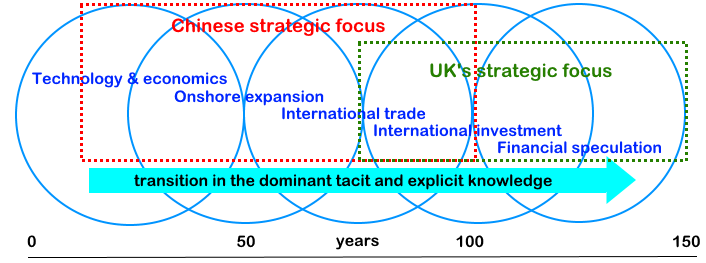

In the diagram of the hegemonic cycle the known universe of the current generations in China are not the same of the current generations in the UK. These impact strategic foci. This is why trying to "compete" with China applying our current known universe of logic based on our capabilities, our "strengths" is doomed to be ineffective if not a complete failure because any competition requires competing on the basis of developing comparative or better processes that make up the strategic focus of the rising hegemon.

1 Locational-State Theory is an advancing and practical approach to analysis of phenomena based on time-space identities. It has application in the analysis of climate change impacts and investment project design and is useful in improving data analysis and understanding the impact of human evolution and events on the state of human knowledge, communications and general semantics (see Locational-State Theory). |

|

|

Today the declining hegemon is the United States and Britain has survived to some extent by remaining closely tied to that country in terms of foreign policy and trade. The rising hegemon is China.

The seminal works by Giovanni Arrighi (1937-2009) in the form of,

"The Long Twentieth Century" providing copious evidence for the significance of hegemonic cycles and, "

Adam Smith in Beijing" which reviews a commonly overlooked detail in Adam Smith's work predicting this evolution.

The diagram on the left shows the typical hegemonic cycle and the characteristics of economic activities over the cycle. The text below the diagram describes a vitally important locational-state concept of "

known universes" and how this impacts national strategies based on current capabilities."

FinancializationSince 1971 there has been an acceleration in financalization, again this is not a recent phenomenon. This is a process repeated over the last three or four centuries involving Venice and the expansion and declines of the colonial periods of the Dutch, Portuguese and the United Kingdom. The normal sequence is progressive loss of value in the currency or purchasing power, inflation in assets and falling real incomes of a significant proportion of the population are all well known and established characteristics of the cycles. The question naturally arises,

"If this is so well known, why don't governments act to avoid the disastrous final phases?" This question has never been given enough dedicated consideration and as a result there has never been an effective strategy to escape the inevitable decline. This is because the generations who initiated the rise in power based on productivity and innovation are no longer alive, most of that tacit knowledge has been lost, that known universe has evaporated. In the middle merchants simply sold more of the same to the world to accumulate capital leading to the financialization periods three or four generations on. The final phases affecting our current generation, see everything in terms of financial management and manipulation, including monetary policy, with far less emphasis of physical productivity simply because of the loss of people with the relevant tacit knowledge relating to "

how do" competence; this has been lost, accelerated by such policies as QE.

The curse of the limitations of the known universe

Since, the late 19th Century the hegemonic phase shaped the known universe of policy makers which shifted towards financial manipulation and away from technological solutions.

A failure to understand the importance of maintaining the technological dimension of macroeconomic policies led to a sequence of financial crises

As a result, some 60 years later the New York Stock Exchange Crash heralded the Great Depression.

Solutions were all of a financial character but introducing financial regulation to prevent speculation.

With the international petroleum crisis, slumpflation combined rising unemployment and cost-push inflation, for which monetary and Keynesian policies had no solution; the issue is technological.

The solution selected was an intensification of financialization and removal of counter-speculative financial regulations, leading to the 2008 crash.

The solution to the 2008 crisis was yet further financialization through quantitative easing leading to a rapid acceleration in the decline of the UK economy which was obscured by the Covid-19 crisis. |

The agents of change"Britannia Unchained" and

"Greater" put some store of value in governments bringing about changes in policies or changing the way democracy works as some part of the solution. This has a logic but it is irrational. This is because our politics is dominated by political parties who in turn are easily captured and controlled by the powerful financial and business sectors who become major benefactors of political parties to gain influence over policies in exchange. Since the interests of these benefactors has become increasingly financialization they have favoured policies that place more emphasis on monetary affairs and which are structures in their interest. With the advent of universal suffrage the influence of benefactors has been extended through the media in order to ensure that political parties and individual politicians are cowed into submission by a media that follows the interests of the financial sector and corporations who have the same "interests" as the media barons and political party benefactors.

Therefore the driving force to create a self-fulfilling advance of the hegemonic cycle is not political parties but the commercial and financial interest groups that impose their will on government decision making and monetary policy.

We were warnedIn the seventeenth century, the Levellers who promoted universal suffrage and a move towards participatory democracy had the sense to try and build in safeguards, into their constitutional propositions, to avoid the formation of political parties and permanent civil service. This was to prevent the build up of corruption and blocks gaining influence over governance. Subsequent key steps in our constitutional development, increasingly in the hands of political parties, sought to ignore these provisions and finally to remove them altogether.

Economic theory and derived practiceEconomic theory and derived policies have been guilty of inflicting severe policy induced prejudice on populations through what has amounted to a series of social experiments mostly generated within an isolated academic bubble dominated by the circulation of peer-reviewed papers in a sort of intellectually incestuous self-supporting reaffirmationary cycle; a never ending exploration within a limited intellectual critical mass. The support of academia in terms of professorial chairs and funding came largely from corporations and the state and therefore the main thrust of enquiry has become increasingly to do with monetary affairs. The direct result has been a limitation of enquiry with the "known universe" of the people concerned being increasingly restricted by the organizations supporting this way of thinking and analytical behaviour. As already mentioned, the focus of people serving society and leadership is moulded by the current generational emphasis. In our case this has been the role of money or monetary policies in managing the economy. In the United Kingdom there appear to be just two saints in this almost religious fold in the shape of John Maynard Keynes and Milton Friedman and a minority sect who give lip service to Friedrich Hayek and yet some others to Karl Marx. Keynes, Friedman and Hayek are all of the generation where monetary affairs were on the rise in the hegemonic cycle. This means their motivation and focus remained on money and finance and their consideration of technology, productivity and innovation was almost non-existent; that known universe pertained to former generations of economists and economic sectors perhaps a century before.

In 1922, Thorstein Veblen made the observation that,

"Half a century ago it was still possible to construe the average business manager in industry as an agent occupied with the superintendence of the mechanical processes involved in the production of goods and services. But in the later development the connection between the business manager and the mechanical processes, has on average, grown more remote; so much so, that his superintendence of the plant or of the processes is frequently visible only to the scientific imagination... His superintendence is a superintendence of the pecuniary affairs of the concern, rather than of the industrial plant; especially is this true in the higher development of the modern captain of industry." |

Veblen also sensed the approaching decadence and speculative dimensions of the rise in the importance of money and finance associating this with a significant change in the motivations associated with finance removed from the real economy. He foresaw the growth in financial manipulation who sabotage and retard, rather than advance technological development. He considered success in the business world to wait on guile,

"The successful man under this state of things succeeds because he is by native gift or by training suited to this situation of petty intrigue and nugatory subtleties. To survive in the business sense of the word, he must prove himself a serviceable member of this guild of municipal diplomats who patiently wait on the chance of getting something for nothing; he can enter this guild of waiters on the still-born pecuniary gain, only though such apprenticeship as will prove his fitness. To be acceptable, he must be reliable, concilliary, conservative, secretive, patient, and prehensile." |

Naturally, Thorstein Veblen was not held in high regard by his contemporary economist colleagues but, just seven years later, the New York Stock Exchange crashed and the rest is well known. Of course the "solution" took some time to work out as the world moved into the Great Depression and the most pressing problem was very high unemployment. The early response in the USA was President Roosevelt's New Deal between 1933 and 1939, which took action to bring about immediate economic relief and reforms in industry, agriculture, finance, waterpower, labour, and housing, vastly increasing the scope of the federal government’s activities to get money into the hands of the newly employed so as to drive the economy back to full employment. John Maynard Keynes later in his book,

"The General Theory of Employment, Interest and Money", published in 1936 essentially set out a economic theory and policy what the New Deal had accomplished. Although lauded as a brilliant new macroeconomic theory and policy the basic model had already been demonstrated under the New Deal.

In terms of the hegemonic cycles at this time, the USA was on the rise and the United Kingdom was initiating a decline. What is puzzling is that the USA was very much at the technological and innovation stages as were several UK industries but Keynes only emphasized the importance of money and in particular the raising of money by government through loans to direct the expenditure of these funds into public works and infrastructural projects to raise employment levels and to generate "demand". The alternative was private companies or individuals raising loans to invest but the scale of unemployment, at that time, was so big it was necessary to have government raise loans.

ProductivityThe 1929 Crash, unemployment and Keynesianism created a premature concentration on finance, money and monetarism as the substantive instruments of macroeconomic policy. This resulted in the contribution of technological productivity and innovation as parts of macroeconomic policy being largely ignored. Inflation and the devaluation of the currency became formally considered to be related to the quantity of money in circulation and this was equated with demand. As a result the vital role of technology in raising purchasing power through rises in productivity and lower unit prices did not feature as an area of study relevant to macroeconomic theory or practice. As a result neither macroeconomic theory nor policy intruments featured any consideration of cost-push inflation. This was because, according to the Quantity Theory of Money, inflation was only considered to be caused by rising demand linked to higher money volumes.

The further decline into monetarismThe formalization of the preeminence of monetary policy as the dominant theme of economics was celebrated in the organization of the Bretton Woods agreement in 1944. This was distorted by the fact Bretton Woods was concluded towards the end of the War that ended in 1945 and there was an overwhelming concern with funding for reconstruction for both those who won and those who lost the war. However, the final decision to base the international monetary system on the US$ was destined to fail. This was because the US economy would not be able to grow at a rate capable of supplying gold-backed dollars to support the needs for global economic growth. It could only do so by printing off more dollars than there was gold to back it up. In other words, to succeed, the USA needed to cheat. As things turned out Bretton Woods did fail in 1971 when countries began to demand gold in exchange for excessive dollar holdings. As predicted there were more dollars in circulation that gold to back them up and Nixon rapidly removed the link between the dollar and gold to avoid having to honour the US undertaking under Bretton Woods (see

"Bretton Woods in retrospect").

Increasingly precarious monetarism Coming off the gold standard only increased the precariousness of monetary policies, worldwide, through the issuance of increasing volumes of money that had no reliable backing (fiat currency).

The failures to embed technology and innovation into economic theory and policy practice as an arms against inflation and monetary devaluation were rudely exposed when existing macroeconomic theory and existing policy instruments were found to be unable to address the rising problem in the 1970s of slumpflation. This was caused a very rapid rise in the international price of petroleum. Policies by that time had no instruments to handle this cost-push inflation combined with rising unemployment. Keynesianism would not work and inexplicably governments opted for a monetarism model advocated by Milton Friedman who based his apporach on a fixation with the Quantity Theory of Money and "demand management" based on money volumes and interest rates. Like Keynes, Friedman had nothing to say concerning technological innovation and real economic growth, so this version of monetarism only exacerbated the state of affairs in the same way as Keynesian instruments. To add fuel to this fire Hayek in his opposition to state intervention and his notion of it being a

"road to serfdom" only encouraged people like Margaret Thatcher place more emphasis on the "private sector debt option" and Miltonian monetarism.

Again, ignoring the significance of technological solutions, the whole process involved the removal of financial regulations introduced after the New York Crash to prevent the types of speculation that gave rise to that crisis. Since the solution was again purely based on monetary policy, the time delay to reach another financial crash in 2008 was just 25 years whereas the time from the initiation of financialization, estimated by Veblen, to be around 1870, took almost 60 years to the 1929 Crash. As from around 1980s the rapid expansion of derivatives and options following Black and Scholes development of a computer-based risk management hedging formula in early 1970s, accelerated the rate of financialization so the next crisis occurred in half the time (30 years compared with 60 years). Once again, because of the known universe effect, the "solution" to the 2008 crisis was to apply yet more intensive financial and monetary policies in the form of quantitative easing (QE). By 2021 the impact of QE was creating yet more problems in the economy. Investment in productive activities fell along with productivity and real incomes of an increasing proportion of the population. Within 15 years this intensification of financialization would have created yet another major financial crisis but was interrupted by the arrival of Covid-19.

This concludes this first article in the series of three.

The second part of this series we will explain how increasing size of the financial sector, under current government policies, can only accelerate the decline in real incomes in our population as a direct result of exclusion of adequate investment and rises in productivity leading to an inability to pay compensatory real wages. It will further set out how the salvation of the economy and wellbeing of the constituents of this country depend upon a movement away from monetarism through a process of devolution of policy decision making to companies and workforces by removing the state and the Bank of England from their dominant positions in policy decision-making. This is not as radical as it might sound. It does not require resort to the imagined solutions associated with either end of the political spectrum as extreme left or right. It is based on what was contained in the "known universe" and more robust economic theory understood and applied by those who ran balanced economies in the more distant past based largely on a devolved and successful basis. At the same time this addresses the unacceptable state of affairs of an increasing social and economic damage associated with our current postion of considering the advance of the final phases of the financial/monetary dimensions of our hegemonic cycle as inevitable. In 1967, Marshall McLuhan and Quentin Fiore in their book, "

The Medium is the Massage" stated,

"… there is absolutely no inevitability as long as there is a willingness to contemplate what is happening."

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2020) unless otherwise indicated