In order to explain the tendency towards income disparity it is necessary to distinguish between two sources of income and then to analyse how macroeconomic policies affect each one. There are two basic sources of income:

- Receiving income as a wage of fee in exchange for work or services provided

- Receiving income on the proceeds of asset transactions and the rise in value of assets held (wealth)

|

Wages consist mainly of cash payments.

Assets include:

- Land

- Real estate

- Precious metals

- Other financial assets including cryptocurrencies, derivatives, shares, loan collateral

|

The article,

"Changing our constitution to establish public choice - Part 1" explored why there are distinct differences in what constitutes a desirable macroeconomic policy depending on whether a constituent gains their income from wages or dealing in assets.

The significance of sources of income

The interests of wage-earners

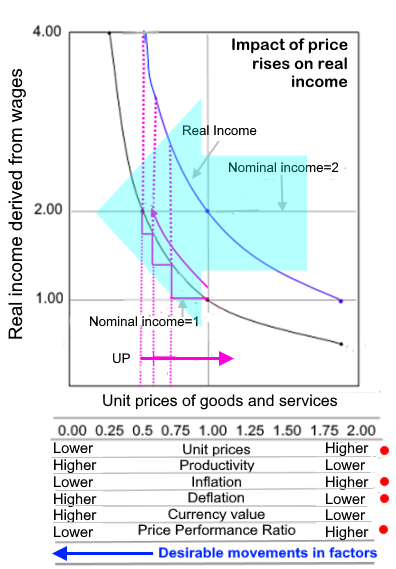

Wage earners benefit from lower unit prices, lower inflation, from increased deflation, enhanced currency value, lower price performance ratios and productivity increases in goods and services production.

Please refer to the footnote on this page. |

The interests of asset holders

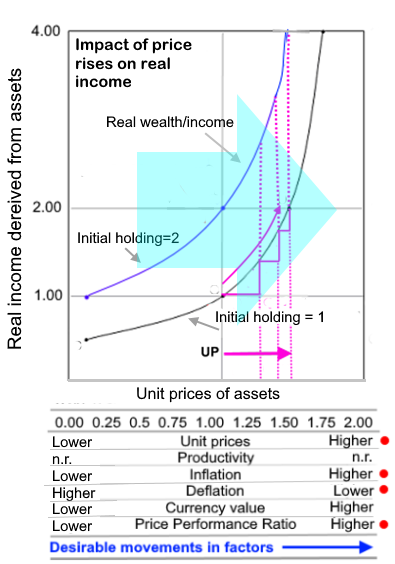

Asset holders benefit from higher unit prices, higher inflation, higher price performance ratios in asset transactions and only a marginal interest in goods and services productivity increases.

Please refer to the footnote on this page. |

As can be seen from the diagrams on the left and right

the specific interests of wage earners and asset holders are diametrically opposed in terms of desired price movements.This can be seen from the opposite directions in which each group benefit from price movements. This is indicated in the large turquoise arrows in each diagram.

Rises or inflation in assets benefit asset holders whereas inflation in goods and service prices prejudice wage-earners. The technological benefits of deflation favour wage-earners while deflation in asset prices prejudice asset holders.

Asset holders enhance their income and wealth by dealing on the basis of price performance ratios that exceed unity (>1.00) whereas supply side production that is able to raise productivity and lower unit prices needs to operate at a price performance ratio of less than unity (<1.00). These significant differences in interests are marked by the red dots

.

Why has policy favoured asset holders?In terms of alternative macroeconomic policies this bias can be resolved fairly simply. However, there are practical difficulties in the United Kingdom in identifying macroeconomic policy to accommodate these differences. In terms of the constitutional economics the democratic concept of public choice as an open system under which well-informed citizens debate, identify and support economic policies considered to be of mutual benefit does not exist. This is because this depends on a system that affords an equivalent weight to constituent interests in analyzing and deciding on economic policy. Under our system, the process of public choice is controlled by political parties that set the agendas that become legislative proposals, acts, laws and regulations. There is a tendency for the party machines to have a bias towards the interests of their main financial benefactors. Since British political parties are so tiny - total membership amounting to just 1.25% of the electorate - they are, in terms of individual member financial contributions, bereft. They are, therefore, easily captured by domestic and foreign corporate financial benefactors ranging from wealthy individuals and corporations to specific interest groups such as unions.

Real Incomes Policy

RIP has two macroeconomic policy instruments:

The PPR is a measure of progress of each economic unit in lowering the ratio between changes in output prices against variations in input costs. The PPL is a rebate on a basic levy according to the PPR values achieved. Economic units can manage their affairs to minimize the levy even to zero. In this way the macroeconomic policy is coordinated by the participatory development of companies and their work forces and not by largely arbitrary interest and debt targets. RIP bases policy impact and success on the knowledge and calculations made by the economic actors thereby solving the calculation and knowledge problem in an operational structure that more closely approximates participatory constitutional economics.

|

|

|

This, to a large extent explains the tendencies in macroeconomic policies that have persisted for the last 50 years favouring the rise in asset values and the steady decline in real wages. This is the result of an over-concern with the valuation in all assets including corporate shares while at the same time, under quantitative easing, diverting money away from productive investment and productivity. As a result shares are no longer a productive investment where the price-to-earnings ratio provide an indication of corporate performance linked to efficiency and productivity. Share have become divorced from productive investment and only serve as a store of value with no relationship to supply side productivity. This is why in the "productivity" row under the assets diagram above productivity is marked by "n.r." indicating not relevant. As is evident, this is completely the inverse of the interests of the majority of the constituency who are mainly wage-earners. The low interest rates under QE has destroyed personal savings while making funds easily accessible to corporations to be used to purchase and trade in assets.

The governor of the Bank of England objected to a title of a report by the Economic Affairs Committee entitled,

"Quantitative easing: a dangerous addiction?", saying "[Addiction] is a word that has a very damaging and very particular meaning to many people who are suffering. But the people who are suffering are wage-earners, the majority, and who remain mystified by the purpose of the Bank's monetary policy. This is the direct result of inaccessible language and isolation of those running these affairs. In a democracy it is important to become concerned with the interests of the majority. The Bank of England's actions do appear to be an obsession with asset values and the inability of the Bank representatives in the media, parliamentary committees and in their releases to explain in clear terms the relation of QE to practical beneficial outcomes for the majority. Because of this, their run of over 12 years imposing QE, which has been so damaging, they have shirked the provision of convincing explanations in plain English, so that constituents can understand. Therefore, this is justifiably interpreted to be a form of an obsession cloaked in, what is for most people, mumbo-jumbo. That the Bank is under pressure to explain and account for its policies is, of course, good. But when provided with the opportunity their statements lack both logic and clarity for most people. For example, in giving evidence to the Economic Affairs Committee there was scant reference to the real economy or wage-earners but rather an alarming statement that the Bank is still learning about the effects of QE after "managing" it for 12 years!! This would indicate that the Bank is without direction because it is too "independent". It would seem to that it needs to be brought back into a position of better oversight and direction to benefit all of the constituents of this country and not just asset holders.

The solutionAssets gain value to the extent that they are production factors in raising supply side productivity associated with reduced price performance ratios. The same types of investment that return corporate shares to levels that reflect their earning capacity and that raise productivity to cut inflation and raise real incomes, are the very same investments that will slow down the wasteful drain of funds from supply side investment. This can help raise real wages. The only current macroeconomic policy proposition that has the potential to achieve this is a Real Incomes Policy which encourages all economic units to reduce their price performance ratios and raise productivity.

Footnote: First of all apologies. The original comparative graphs placed on this page had price axes moving in opposite directions (assets on one,

and goods and services on the other) this is how we work internally with these graphs.

However, in that form they caused some confusion on the part of readers and therefore a poor transmission of the essential message. This message is that each constituency group's interests are diametrically opposed to one another. This is why any slight bias in policy to one or the other will cause significant cumulative benefit to the interests of any particular group over time i.e. asset holders or wage-earners. The last 50 years have winessed a continual two-generation run in macroeconomic policy favouring asset prices and asset holders. This has accelerated under quantitative easing (QE) during the last 12 years. RIP enables this distortion to be removed to enable a movement towards a more balanced distribution of benefits.

1 Hector McNeill is director of SEEL-Systems Engineering Economics Lab

All content on this site is subject to Copyright

All copyright is held by © Hector Wether ell McNeill (1975-2021) unless otherwise indicated