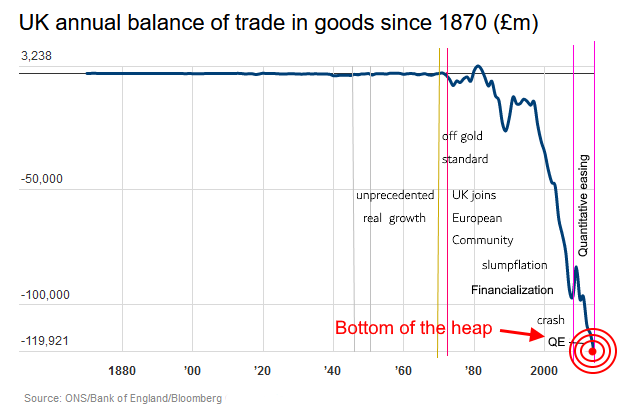

Where we areIn terms of our position in the international league table for balances of payments, we come second from the bottom. The grand prize for an even worse balance of payments, goes to the USA.

As can be seen from the diagram on the left, our economy sits at the base of a precipice, see the point surrounded by red concentric circles, of declining competitivity which started around 1981.

This tells us that others are not buying enough goods manufactured in this country, others are producing better and cheaper products. It also informs us that we are importing large amounts of our requirements for goods from abroad including essential foods.

This was not always the state of affairs given that the global leadership in initiating an industrial revolution was gained by Britain a country that became "

the workshop of the world" starting out on this journey as far back as the eighteenth century. The balance of payments remained in balance for most of the period between 1870 until 1970. The balance hid increasing amounts exported and imported goods reflecting growth in real consumption supporting a rising standard of living. Between 1945 and 1965 Britain had an unprecedented growth rate, maintained industrial investment and rising productivity, saw a declining income disparity and rising real wages and, throughout this period, full employment.

The 1973, the OPEC decision to raise petroleum prices initiated

a period of financialization greatly intensified by the recycling of petrodollars. Much of the investment using funds from the United Kingdom were redirected into offshore investment in low income countries. This resulted in a decline in investment within the United Kingdom in strategic industries and manufacturing leading to a widespread de-skilling of the workforce, rising unemployment and declining real wages in a shrinking industrial sector.

A book published in 1960 entitled,

"The Stages of Economic Growth" by Walt Rostow, used the economic growth stages of the United Kingdom as a "model" where industry had become a secondary sector to services in terms of the numbers employed. This stage, as far as Rostow was concerned, was the final stage of development a sort of peak or plateau, referred to as the stage of mass consumption. However, it is evident that Rostow did not reflect on the evidence concerning so-called hegemonic cycles of former colonial countries, like Britain. These, including the Venetian, Spanish, Portuguese and Dutch hegemons, had all been industrial economies, which began to export their production and accumulate money which was then applied in overseas enterprises, as was now observed in the last 40 years in the United Kingdom. The result, in all cases, was a rising intensification of financialization, structural inflation and economic failure. None of this, of course, was included in Rostow's book because by 1960 Britain was still expanding its service sectors. The event that launched Britain into the final period of financial chaos was OPEC's 1973 decision to raise the international price of petroleum creating stagflation, a condition that endured for 20 years.

Monetarism's debt-taxation trap

The disappearing "headroom"

The over-reliance of monetary policy instruments such as interest rates and the legacy of quantiative easing is likely to land Britain with debt interest payments of around £120bn creating an enormous strain on attempts to tackle COLIC by coventional means.

The latest Office for National Statistics (ONS) data show this to be the case. Borrowing in July 2022 was Ł4.9billion higher than predicted Ł200m spring figure. Debt interest payments rose by £5.8billion and cost of living assistance raised this by another £2.2billion.

Since the start of the financial year Britain has borrowed Ł55billion some £3billion more than OBR forecasts. Higher debt interest payments, are around 25% of the national debt, now at £2.4trillion, linked to inflation.

Total debt interest for 2022-23 is about £35billion higher than the Ł83billion forecast by OBR. Higher interest rates will boost this to around £118billion. The servicing of national debt exceeds the budgets of many departments including defence.

Liz Truss's proposition to reverse national insurance hikes, scrap green levies on energy bills and Ł10billion additional support could raise annual borrowing to £170billion.

The latest official data suggest that the £30billion "headroom" is likely to be used up. This will leading to an increased borrowing requirement in a repeat of the state of affairs in 1975. However, Liz Truss is indicating a desire to provide £30billion of tax cuts. It is unlikely that this will be possible.

We face rising inflation, rising debt the inability to lower taxes or provide more support to constituents and the BoE seems to be intent to follow an ill-advised trajectory of rising interst rates.

Monetary policy is backing the country into an increasingly perilous but inevitable deepening debt-taxation trap.

There is therefore no other option than to tackle inflation head on by non-monetary means as a priority to reverse rising prices.

The only policy designed to achieve this in an effective and timely manner is a Real Incomes Policy. |

|

|

The Keynesian and Monetarist miragesFollowing the Great Depression, caused by a mismatch of what was produced to what was needed and initiated by the New York Stock Exchange crash of shares funded on excessive debt. This resulted in a depletion of cash flow caused by a massive repossession of collateral held by banks, John Maynard Keynes published his book,

"The General Theory of Employment, Interest & Money" in 1936. Even before his theories were adopted, several countries were recovering based on the former model of growth based on companies growing by improving productivity through investment and selling more competitively prices goods that were accessible to relatively low income populations. In Britain the period 1945 through 1965 the economy expanded rapidly and because there was full employment, no Keynesian policies were applied. It is odd that studying economics at Cambridge in the 1960s, Keynes former base, the courses were waterlogged by Keynesian theory concerning the role of government in "recovery" when, at that time, recovery was occurring without any specific help from Keynesian p[olicies such as government loans and expenditure. The economy was expanding "on its own" and government revenue and national accounts were in surplus.

Production and investment strategies were reviewed under a tripartite system involving committees attended by representatives of government, trade unions and industries as employers. The UN International Labour Office did much to promote this type of dialogue as a basis to avoid conflict and divergence of interests by maintaining a focus on human rights to created a forum characterized by mutual respect between parties and a focus on national interests.

Naturally under the situation of confusion caused by stagflation resulting from cost-push inflation linked to petroleum input prices, intense financialization spurred on by petrodollar recycling and accelerating offshore investment creating unemployment, any tripartite operation would have been impossible. The initial impact of stagflation was to upset Britain's balance of payments. It so happened that the Treasury significantly over-estimated the government borrowing requirement and in panic Denis Healey, the Labour Chancellor, switched from Keynesianism and a wages policy to monetarism in 1975 and ended up requesting an unneccessary loan from the International Monetary Fund (IMF) in 1976.

Monetarism was enthusiastically embraced by the following Thatcher governments and by 1981, the government introduced a budget that motivated some 364 economists to sign a letter to the Times newspaper stating that the combination of supply side economics with monetarism would depress industry and raise unemployment. However, this letter was not accompanied by any alternative propositions. I therefore circulated a monograph on the Real Incomes Approach to the leading political parties (Conservative, Labour and Liberals) to at least present an option. By that time the dogmas of supply side economics and monetarism had taken hold as the flavour of the period causing any alternative proposals to be given short thrift. The outcome of the 1981 budget, as predicted in the Times letter, was bad and by 1990, as a result of injuriously high interest rates, house repossessions peaked in 1990. The balance of payments began to tumble and unemployment rose. I therefore decided to run a survey, funded by the Manpower Services Commission, of 100 leading companies in Hampshire County. This survey enquired as to their possible interest in an Onshore Engineering Club to begin to analyse how to bring investment back to Britain to begin to re-skill work forces and initiate an industrial recovery linked to digital technologies. Only one company showed any interest and on visiting the company, in Havant, the representative did not comprehend the issue and had no decision making power.

Nothing worksIt had been evident since the mid-1970s that monetarism and Keynesianism offered no solutions to stagflation. The reason is fairly simple. Keynesianism and monetarism both consider inflation to be linked to excessive demand and therefore their principle policy instruments are designed to influence demand. Broadly speaking this paradigm is referred to as the Aggregate Demand Model (ADM). However, stagflation was caused by cost-push inflation. Therefore Keynesian and monetarist policy instruments could not affect this type of inflation. The same is true today with policy instruments having undergone no revision or additions. The arguments between Keynesians and monetarists in the 1970s on how to control stagflation were largely redundant and the fact that monetarism seemed to win the argument only meant we remained with a policy domain offering no rational solutions.

So, what worked?It is self evident that an inspection of the balance of payments indicates that the performance of the economy has been declining since around 1973. Successive variants of monetary policies combined with supply side elements, in the UK, at least, have simply contributed to this decline. The opinions on the effectiveness of so-called supply side economics are varied. Bill Clinton, in a lecture to Georgetown University in 2014, outlined a particular crticism of supply side (see:

Some evidence on the failure of supply side economics). Therefore, the question becomes, "

In the past, what worked?". It is very apparent that attention needs to be paid to what maintained the extraordinary growth in economic expansion experienced by the UK since the eighteenth century, through to 1965. Wars and recessions apart, the motor was corporate own investment and competitive pricing, money was not the dominant factor in policy but maintained its role as a facilitator of enabling the buying and selling of goods and services of very different types as well as a holder of value or liquidity in the form of savings. The mistake made by Keynes was to consider savings to be a factor that created a deficit in demand because they were not spent. A hint to this thinking can be found in the so-called Cambridge Equation, a version of the defunct Quantity Theory of Money (QTM) to which he contributed. Here it is evident that higher savings reduce the overall weight of money in the economy used in transacted goods and services. Thus:

The QTM identity based on Irving Fisher is as follows:

M.V = P.Y ... (i) and the Cambridge Equation based on contributions from Keynes, Marshall & Pigou, is as follows:

(M-s).V = P.Y ... (ii) Where: M is money volume; s is savings; P is average prices and Y is income spent.

Note that the Cambridge Equation is slightly different from the original to create a format that is of the same structure ad the Real Money Theory to facilitate comparison (see below).

The oversight made by Keynes, and most other economists, is that the QTM does not in reality represent what is happening to the quantities and prices of goods and services. Universal suffrage brought to the fore the primary concern of constituents as being the cost of living. This is determined by the prices of goods and services compared with their incomes. Before such concerns became a major consideration of politicians, the main interest of policy was to maintain the value of assets held largely by the power brokers and those controlling the political elite. The Real Money Theory (RMT)

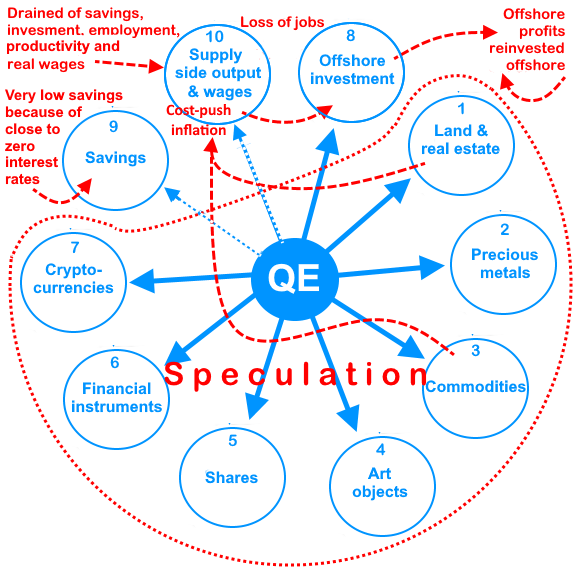

2 is an extenson of the Cambridge Equation which adds in all of the main asset markets as variables and which are missing from the QTM and Cambridge Equation. One version of the RMT is presented below.

M - (s + l + r + p + x + f + c + a + m + o) = P.Y ... (iii) Where: s is savings; l is land; r is domestic and commercial real estate; p is precious metals; x is shares; f is financial assets; c is crypto-currencies; a is rare objects (art); m is commodities and o is funds flowing overseas into offshore activities.

MONETARY POLICY

The induction of speculative asset price rises

Supply side and constituent marginalization.

|

This exposes the fact that savings are a marginal element in impacting "demand" and that assets and leakage overseas are of more significance in reducing consumption or what Keynes would have referred to as "demand". This was made very evident during the 12 years of quantitative easing (QE) when each tranche of QE funds raised the prices of assets almost in direct proportion to the relative sizes of the advanced funds. The prices of goods and services were impacted later in this story as described in Part 1 of this article. The result was a significant rise in the wealth of asset holders and traders who, gained directly from this policy. Also the main savings activity was to be found amongst asset holders and traders in in spite of QE being associated with close-to-zero interest rates. Certainly, those of average wages were not saving money because real incomes were declining as a result of shrinkage in the goods and services markets caused by the diversion of money into assets and interest rates or returns on saving were too low.

As can be appreciated, this whole monetary approach is misleading because the main beneficiaries of monetary policy, through the ages and now, have been a tiny faction of the national constituency, probably constituting no more than 5% of voters. The QTM, as the RMT shows, as the rationale for monetary decision of money volume based on debt or interest rate policy never served the interests of the other 95% of the constituency.

What always served the interests of the majority has always been the steadfast growth in business physical productivity or more-for-less and competitive pricing. This has always resulted in wage-earners, even on fixed wages, seeing their purchasing power rise a lá 1945-1965 and most of the period of the industrial revolution phase lasting over 150 odd years up to 1965. This period has come to be referred amongst world systems and hegemonic studies as the "long century".

This area of research, and the majority of evidence it has exposed, demonstrates that the reliance upon policy decision making that results in higher volumes of money simply prejudices the population by draining away the potential benefits that come from rising industrial and manufacturing investment and productivity conbined with competitive pricing. The focus needs to remain on the real incomes outcome for the majority. In this context, what works is policies that either leave companies alone or which create incentives to help companies execute this function more efficiently and involving less risk.

More to SayAt the beginning of Britain's long century, in 1803, the French economist Jean-Baptiste Say, one of the most enthusiastic supporters of Adam Smith's approach, explained in his Economic Treatise how wealth is produced, distributed and consumed. In terms of growth he pointed out the importance of the process of entrepreneurialism as that process whereby observant individuals identify ways to increase the efficiency with which resources are use to create goods. This resulted in such enterprises serving the interests of consumers by making products more accessible as a result of competitive prices. An associated effect of competitive prices was the fact that expanding penetration of the market increases volumes of sales as operators become increasingly skilled in their production, committing fewer production errors, creating less waste, taking less time and gradually lowering unit costs. A vocational professionalism associated practical experience sustains an constant evolution in inovation and productivity created a sense of accomplishment and increased dedication to refining the art of production. As a result, what was of enormous benefit to consumers became the prime interest of producers combining the ability maintain a compensatory income while contributing to the evolution in real incomes or purchasing power of consumers across a widening array of goods and services.

Jean Baptiste Say's logic extended to explaining that this live relationship between producers, those employed by production units and who were also consumers, signified that the efficiency and wages paid in production units constituted the sum total of demand in the economy. As long as the trajectory of production is characterized by rising productivity and competitive price setting there will be real growth because the wages can purchase more real goods and services. What will undermine this process is economic policies that take money as the controlling factor by imposing centralized top-down dictats concerning interest rates or the use of taxation. These policy interventions break the beneficial one-to-one relationship between wages and salaries paid as the determinant of consumption levels or demand.

Since 1975, in Britain, this is the direction in which economic policies have moved following the complete misdirection led by the evangelists of monetarism such as Milton Friedman and interventionists, advocating top-down money volume control and centralized direction by government, such as John Maynard Keynes. The widespread following amongst loyal economists of both monetarism and Keynesianism, and their ability to ignore the fact that goods and service production efficiency and prices remain central to the wellbeing of the constituents of this country, has led to advice encouraging governments to dictate terms and conditions which, in practice, have been a disaster. We face a problem of so many high profile individuals representing these camps consisting of a whole ecosystems where thousands of economists gain their incomes, not from producing goods but rather by advocating policies which undermine the essential conditions for economic success. In reviewing the RMT it is evident that the headline policies that this country has implemented since 1975 to 2022, a run of some 47 years, have favoured asset holders and traders. These are the very same groups who support political parties, many think tanks and academic chairs in economics at universities. As a result the momentum and pecuniary interests of all involved depend upon this pack of cards remaining in place at the expense of the majority of constituents.

Today we face a serious problem of self-censorship in the media which is becoming increasingly controlled by so-called high tech companies with most constituents gaining their news from social media. It has become a fact that those who question mainstream narratives can have their platforms on social media switched off or removed (canceled) as a result of censorship. This is completely against the constitutional principles of early values as expressed in the inspiring attempts to write English constitutions in the seventeenth century, designed to liberate the people of this country to be able to pursue their own objectives and to establish laws to ensure that no one can pursue their activities in a manner that prevents others from securing theirs. Such objectives include the right to expression of free speech addressing any topic and, above all, subjects of importance to the general wellbeing of the majority and, by implication, the nation.

Policies and the adherents of interest groups within politics and the media have created a state of affairs that is on a pathway of destroying freedom of expression and liberty. Today, many have become afraid to call attention to outrages because of fear of becoming conspicuous for rebelling against them. This is unacceptable. On the topic of COLIC we can continue to exacerbate the situation for the majority of the population by pursuing policies that have no transparent theory but are simply ideological concepts. There is a need to stop fooling ourselves, linked to selfish personal interests, ideological beliefs and accomodations that harm others, and, through highly selective self-serving "evidence". This political, academic and media corruption of the very data, information and knowledge we need to begin to serve all our interests requires a more robust intervention of informed public choice. Public choice is the constitutional principle of participatory development of policies involving the electorate by providing insight into the cause and effect relationships on policy propositions as a basis for constutuents to have influence over decisions that affect them. Political parties resist such common sense by claiming economics is too complicated for those who work to produce goods and services while they impose policies that undermine these very functions of these constituents. It is self-evident that some form of tripartite arrangement between government, employers and unions is required, as existed in the early post second World War years, at least to initiate a forum for objective analysis linked to clarifying the mechanisms of cause and effects contributing to stagflation.

What should not be ignored is the damaging impacts of our recent foreign policies in undermining the state of affairs as a result of the global impacts of the ill-advised sanctions regimes which have impacted us more that the countries targeted by sanctions. The intention of the Bank of England to continue to raise interest rates is another extraordinary state of affairs which has reduced this institution to a destructive loose cannon. Largely overlooked, foreign policy and the question of BoE independence and dominance over macreconomic decisions, are topics that should loom large in any tripartite deliberations.

How to serve the interests of a nation

Companies and work forces need to be released from the straight jackets imposed by monetary policy and taxation and they should be provided with incentives to become more efficient and gain the levels of efficiency in price-setting to kill off inflation. However, there is a need for an additional effort to get the economy back into a state of operation following the Say model. Real Incomes Policy (RIP)

3 provides incentives for companies to begin to reduce the prices of goods and services in the short term so as to immediately impact all. In particular, low wage earners would benefit by rises in their purchasing power. RIP helps companies lower their risks and gain from lowering unit prices by making up for reduced margins in return for the actual price reductions that are implemented. This, therefore, removes the major waste associated with state grants and tax super-deductions associated with "investment" for which no proof of raised productiviy or real gains are provided. In this way the tax revenue forgone by government is quantitatively reflected in an across the board immediate rise in real incomes and real national growth in a counter-inflationary policy. Lowering unit prices in this way expands the sales of companies resulting in employment rising in an environment of rising real wages affecting increasing numbers of constituents. Over time such incentives can be reduced because production efficiency will attain sustainable levels on a more-for-less basis. This the essential operational structure in support of planetary concerns with respect to climate change and natural resources carrying capacity.

FreedomOur future as a free nation of individuals depends upon each person's ability to manage their affairs without arbitrary policy impositions that constrain our self determination to shape our individual futures according to our own wishes while not imposing on others. This ability rests on an equivalence between our efforts and compensation received in terms of our real incomes that determne our personal ability to access the resources we need for advancement.

1 Hector McNeill is director of SEEL-Systems Engineering Economics Lab

2 "Why the Bank of England cannot solve the cost of living crisis", BSR, 2022.

3 For a more detailed explanation see: "Monetarism & The Cost of Living Crisis", BSR Special Edition, 2022.

For a historic review of where policies have gone wrong it is well worth watching the video of a presentation of Steven Kates to the Mises Institute, under the title of: "Why your grandfather's economics was better than yours."

A working paper posted on Cambridge Economics Network sets out the specific contributions of the Real Incomes Approach to economic thought and analysis establishing it as a separate alternative to Keynesianism and monetarism and a distinct school of economic thought: Contributions of the Real Incomes Approach to economic thought - A resumé

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2022) unless otherwise indicated