Hector McNeill

1

SEEL

The disintegration of an economy can take place quickly as a result in the differentials between monetary flows in to different asset classes. The 50 years of financialization and the last decade of quantitative easing (QE) have provided a transparent case study of the destruction associated with these facts.

In spite of this evidence, economic policy discussions fail to distinguish between assets classes so the lessons are not learned.

|

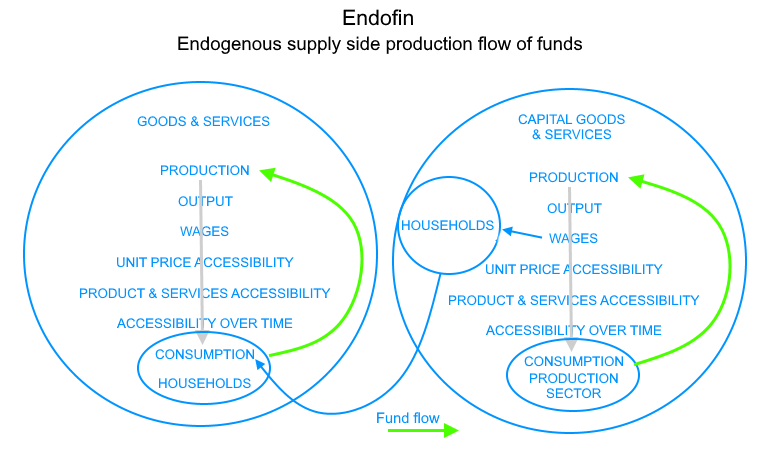

IntroductionIn the Say model of the economy a state of equilibrium with gradual real growth resulting from of innovation and price setting making products and services more accessible to wage earners and others. In this model disposable incomes established the consumption of output and incomes were paid by the supply side whose output is paid for by the disposable income. Here Say's Law can be seen to rule.

Under such a system the significant assets are the

core productive assets which consist of inputs materials, productive plant and machinery and human resources, or human capital. At the same time, those who have succeeded in being able to withdraw funds over and above what is required for essential needs, in the form of saving could purchase

non-core assets such as land, real estate and gold. These non-core assets can become productive assets through rental, so earning income from others. They can also be used as collateral to raise loans.

Corporate shares are another asset which are productive in the sense of yielding a dividend based on the work of others. The price of a share was formerly related to the productivity and prospects of a company which determine the likelihood of dividends paid by companies rising or not. This was summarized in the price/earnings ratio. Within the Say model therefore core productive assets generate the income with which land and real estate prices and rentals (agricultural land, houses, offices, warehouses, parking areas, industrial units) and dividends are paid.

Back to basicsThe factors of production (inputs) consist of:

- Objects derived from natural resources (formerly referred to as land)

- Capabilities derived from human resources linked to physical and logical facilities (formerly referred to as labour)

- State-of-the-art processes in the form of technology and techniques (formerly referred to as capital)

In terms of human survival, peaceful co-existence, general satisfaction as well as maintenance of the levels of consumption, it is necessary for personal incomes to be at levels that maintain consumption levels. On this basis technologies become more refined over time as do the capabilities of the workforce leading to innovation and rises in productivity of processes leading to rising real incomes as a result or lower unit prices of enhance wages. Future sustainability of the economy therefore depends upon relative unit price reductions and/or relative rises in nominal wages.

Peter Drucker

1909-2005

Credit: Jeff McNeill |

Joseph Schumpeter

1883-1950 |

Therefore, the central factor in managing consumption or what monetarists refer to as "demand", is the nexus of technological productivity and employee wage levels.

In terms of the national economy it is reasonable to refer to Joseph Schumpeter's opinion of the roles of profits for a nation and these were as a guarantee of future operations (survival of the economy) and employment (maintenance of income, consumption and demand). His central message is that innovation is the key to human betterment, and most dramatically betters the lives of the least well-off. Peter Drucker in a now famous Forbes cover story, posted in 1983, states that Schumpeter's key contribution was to ask the right question. Keynes’ main question during the Great Depression had been how to return to equilibrium. In contrast, Schumpeter's right question was how innovation moves us away from equilibrium toward better lives.

Innovation has a

precursor formative element as well as a

resultant element. The precursor is the management of human capabilities to transform or replace an existing technology into a more productive one. This occurs by individuals being provided with the opportunity and conditions to develop their capabilities through experience of repetitive activities and building up their tacit knowledge on the basis of the learning curve. Associated with this process is the collection of performance information and its analysis and the communication of new improved concepts or designs based on explicit knowledge. The resultant element is the impact of the new innovation on real incomes growth linked to the changes in unit costs, unit prices, nominal wages and profits. Notice that the driver of the economy is the consumption derived from wages paid by supply side consumption goods and services and by supply side production of capital goods for other supply side activities (see diagram below).

Financialization & quantitative easingAs a direct result of 50 years of increasing financialization and 12 years of quantitative easing, wages, as a driver of consumption/demand, have been substituted by the policy instruments of money volumes and interest rates where money has increasingly been diverted into assets and, in relative terms away from innovation and investment in higher productivity. As a result the real value of wages has fallen and with this consumption. Monetary authorities have increasingly referred to share prices as a measure of "economic performance" when in reality the diversion of very cheap money into share buy backs has resulted in dividends having no operational relationship to share prices which are in a speculative bubble. The speculative rises in land and real estate prices is raising costs for families as well as supply side production units through higher prices and rentals while supply side turnover and disposable incomes are declining. As a result, quantitative easing is hollowing out the economy.

Not all assets are an assetIn the quest to secure a balanced economy there is a need for any monetary expansion to be channelled to those activities that maintain the growth in productivity at levels which can also maintain the growth in sustainable real incomes, or wages. Thus the core-asset of human resources needs to be the centre of investment calculations. Financialization and QE have destroyed this priority as investment becomes more closely aligned with shareholder value when most shareholders are not employees. The close operational link up between shareholder interests and executive bonuses with share "options" means the "asset value" of shares has taken precedence over profit, dividends and wage levels, leading to a decline in production capacity of companies. Today over 50% of the large corporate share prices are the result of central bank injection of money and corporate financial instrument purchases. During the last 50 years, many leading engineering companies laid off engineers and employed increasing numbers of financial experts and lawyers and as a result several of these companies today are in survival mode as a result of central bank support. The often criticised Soviet style central administration of paying companies for their production at the end of each financial year has reappeared as a central bank monetary policy paying companies for not producing anything but the issue of bonds and dubious financial instruments which have been purchased by central banks. As a result, the notion of profits guaranteeing sustainable production and employment associated with decent wages has been undermined as product and service markets have been weakened through lack of consumption or what monetarists refer to as "demand".

1 Hector McNeill is the Director of SEEL-Systems Engineering Economics Lab.

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2020) unless otherwise indicated