Hector McNeill

1

SEEL

Mark Carney, the ex-governor of the Bank of England delivered this year's BBC Reith Lectures, moderated by Anita Anand. The Reith Lectures were inaugurated in 1948 to mark the historic contribution made to public service broadcasting by Lord Reith, the corporation's first director-general.

Mark Carney attempted to grapple with difficult issues and addressed the main themes facing us today. However, his approach avoided placing much onus on the gaps in economic theory or policy effectiveness that helped shape the multiple financial crises during the last century. The yet-to-be-defined concept of the market was referred to often in the relation to value and values, morals and sentiments. The normal failure of a monetarist to link wage rates to consumption and overall economic growth was apparent. This was lost in an academic discussion concerning "valuation of people". In terms of climate change and any green initiatives, real incomes remained notably out of sight and emphasis lay in the "work in progress" to be addressed in several international forums whose levels of abstraction have been demonstrated to result in no effective action on the ground.

These lectures were troubling because of the important factors directly related to the continuing negative impacts of monetary policy which were not addressed.

|

IntroductionIn a four part lecture series delivered by someone who has remained at the centre of monetary policy for some time I had expected some lessons learned pointing to some tangible and transparent solutions to our current predicaments. The reason this was not delivered became evident from the evolution in content of these lectures. Mark Carney, in his first lecture essentially repeated the contents of a lectures delivered by Alex Salmond at in 2013 and 2015 concerning the moral and economic philosophies of Adam Smith in keynote economic speeches to Princeton and Beijing Universities in 2013 and Glasgow University in 2015. Salmond used the twin examples of Smiths’

The Wealth of Nations and

The Theory of Moral Sentiments to argue that sustainable economic progress must be linked to social progress. Politics is about people, individuals and families, after all.

Because Carney did not anchor his analysis on the family, the rest of his lectures took on an institutional macroeconomic format at a higher level of abstraction, so awkward things like income disparity and the ongoing ravages of quantitative easing were passed over; serious issues were not really addressed in practical terms.

In the second lecture Mark Carney covered the lead up to the 2007 crisis. He did refer to fraudulent behaviour but he did not really address how such criminal activity continues and be facilitated by quantitative easing, the "solution to the crisis", over the last decade.

His suggestion that by making financial service leaders "responsible" for the behaviour of their employees, as representing a solution to the predicament, is really quite worrying naive. Or was this just virtue-signalling on his part? After a decade of abusive behaviour and use of loopholes, the people concerned are not going to change their "culture" on the basis of being "encouraged" to re-establish any additional weight to ethical decision-making, unless of course this is a mirage used to drum up additional business.

The temptation for leaders to tolerate sharp practice and crime in any economic activity depends upon the tension between

ethics, the law and prudence. Ethics is essentially what orientates decisions in the judgement of the treatment of people's interests with ramifications for the community conscience's judgement as what is fair and just. This can have religious connotations. The law establishes enforcement regulations that demarcate expectation of behaviour guided by various forms of expected due diligence to be observed when taking decisions. Part and parcel of law and regulations are the sanctions applied to those who transgress legal requirements. Prudence is what is of interest to the decision-maker or company. The general outcome of fraud is that people lower down in the organizations are made examples of through fines and prison sentences while the corporations concerned are sanctioned with absurdly low fines, some constituting no more than petty cash. As a result the decision making process under such a weak regulatory and sanctions regime is that the cost of gaining £2billion through fraudulent means is well worth it when the fine is £2million. So when noncompliance with the law becomes a "cost of doing business", ethics evaporates and prudence feeds greed, all facilitated by the financial regulatory regime. A large proportion of the financial service company owners and traders are there to make a killing in as short a time as possible, so let's not be naive about how to manage their negative impact on families and society at large.

The QE undercurrents

In terms of political party fortunes in the power game, there is no doubt that opting for QE would favour increased cash flow gravitating towards the Consertvative party.

On the other hand, a people's QE would probably have saved the Labour party in the 2010 election, since the doling out of QE money to the public would have had to have been assigned more directly by government with parliamentary agreement. QE, as introduced remained in the hands of the Bank of England and its main stakeholders, banks, venture capital funds and others.

Gordon Brown probably did not realise, when he made the Bank of England "independent", in reality to avoid the government being saddled with blame for high interest rates, a la Thatcher debacle, only to find its "independence" meant a loss of government control over monetary policy. Leading to our current predicament.

An interesting passage at the end of the second lecture touched on this topic:

Anita Anand: "We can now talk to Lord Jim O’Neill. Now, Jim, just to remind you, some of you may know him from the House of Lords but also worked for Goldman Sachs as Chief Economist". "...a politician once said to me, “Oh, economists, you know, they have predicted five of the last three recessions,” and so there is a disconnect between the politicians and the economists, and the economists themselves, I’ve heard it many times, and maybe you have too, that politics is kind of a breed below....."

Lord O’Neill: "There is a class below economists…?!"

Mark Carney: feigns surprise....

(laughter).

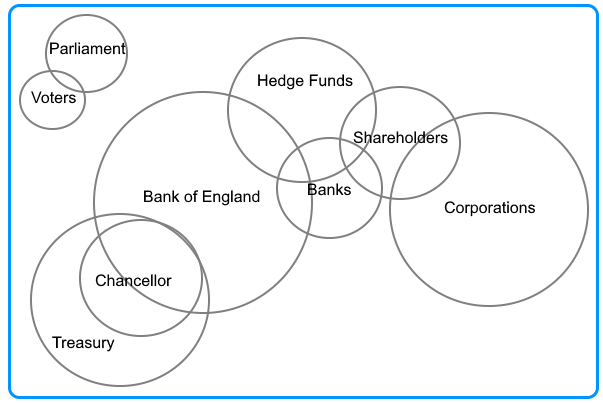

A recent representation of the lack of parliamentary control over monetary policy and the ex-Goldman Sachs economists running it, is reflected in the power diagram below:

Reference: British Strategic Review, 2020

|

|

|

The third lecture didn't really go anywhere but repeated the now universal mantra that Covid-19 experience is imposing conditions that will require a "re-set". But here the emphasis is on

"... in what direction to financial services need to move?" when the question, perhaps, should be,

"... what policies need to be introduced to terminate the continuing monetary policy-induced rising income disparity?" It needs to be admitted that income disparity levels had been driven to totally unacceptable levels before Covid-19 arrived on the scene. Yes Covid-19 highlighted this state of affairs when it was "discovered" that most families had no savings or are hopelessly burdened with debt. Surely a monetary policy issue. This state of affairs is now affecting the whole world and not just the United Kingdom.

The fourth lecture looked to the "re-set" future linked to addressing climate change. Climate change is a symptom of the impact of a growing human population and the technologies they apply on carrying capacity of our planetary natural resources. Since Agenda 2030 was launched in 2015 with 17 Sustainable Development Goals and over 230 indicators to measure progress things have not worked out well in spite of the "talk" by governments, corporations and central banks. Therefore, before the notion of re-set motivated by Covid-19, the 2019 Sustainable Development Report showed that the form of economic growth being pursued (monetarism and quantitative easing), worldwide income disparity in low income and so-called developed countries, has reached unsustainable levels. There has been no advance in sustainability in production or consumption and climate change and rises in temperature continue apace. Over 65% of the indicators for Agenda 2030 production and consumption sustainability and for climate change have not yet been specified after 5 years of "progress".

In his first lecture, Carney referred to Friedman acknowledging that a company might devote resources to provide amenities to its community, but only in the expectation of attracting employees, and that it could engage in such hypocritical window dressing by calling this social responsibility lest it, and Carney quoted, “

Harm the foundations of the free market to admit that this fraud was all in the pursuit of profit alone.” Carney added that

"This is how corrosion happens, and did happen in the ensuing decades.". Unfortunately we now risk the same danger with respect to climate change and sustainability in general.

Gerald M. Meier (1923-2011) of Stanford University wrote

2,

"An economist is both a trustee of the poor and a guardian of rationality." He remained concerned about the distance between them. "As trustee for the poor, the economist respects the values of altruism and economic justice. As guardian of rationality, the economist respects self-interest and efficiency. But does not the future course of development depend in large part on the capacity to combine the seemingly incompatible values of the trustee and the guardian? Can the professional developer combine a warm heart with a cool head?" Our problem, it would seem, is that cool heads have been applied by decision-makers who have no concern for people but only their own interests and status.

Carney refers to Friedman's analysis of the opportunities for the manipulation of public opinion as a way to gloss over the underlying motivation of those chasing money and who, in reality, have no concerns for those needing opportunities to better their welllbeing. As a fellow monetarist, Carney treats Friedman well, but Friedman and other Chicago monetarist's contributions to social outcomes have been a disaster largely as a result of their success in selling their assertions to ignorant politicians, rather than any deployment of rational logic placing the wellbeing of all at the centre of policy objective priorities. Carney referred to financial service bosses becoming "clubby" which became a problem. But if any group is "clubby" and strenuously exclusive, it is the monetarists. The scary part is that most are highly academic in the sense of the word being "not applied". However, their logic does seem to apply well to asset holder's interests but remains purely academic as far as the interests of wage earners are concerned, the majority of the constituents of the country. Soon after his retirement as governor of the Bank of England before Mark Carney, Mervyn King, ventured such a opinion.

When it comes to the monetarist's universal close-to-sacred "explain-all", the Quantity Theory of Money (QTM), they have yet to admit that it is in fact wrong. Quantitative easing failed and exacerbated austerity because the QTM identity does not include savings, assets or offshore investments

3 that have drained money volumes from the supply side production and service sectors so as to depress investment and ability to pay adequate wages and thereby driving down consumption. Or, in the words of monetarists, "demand" is too low. Pumping more money into the economy to raise "demand" just makes matters worse because wages are too low. In other words the whole concept of quantitative easing was misconceived and all predictions were wrong.

In covering the Covid-19 experience in his third lecture, Carney avoided reference to the parallel between payments for furlough and assistance to SMEs and the former proposals for "peoples' QE" in 2007. Covid-19 placed the government's back against the wall so as to force them to run a mini QE for people; this has worked and it is likely to have been a better solution in 2007 and by now we might have had a better recovery. At the time is was the banks who placed the government's back against the wall to secure QE, just for them. The question answer session between Alistair Darling and Mark Carney confirmed this detail of the decision-making during the crisis, but why was the government's focus only on the welfare of banks when, first of all they created the crisis, and a people's QE would have been more effective. Without any doubt it is the presence of the "independent" Bank of England in the discussions that pushed things in the direction of the consolidation of institutional interests and power, rather than attempting to consolidate the real incomes of the national constituency. That would have been too messy and would have involved too government decision making. It is in such decisions that it is easy to detect monetarists blind spot concerning the role of wages in establishing levels of consumption and economic stability. This is too close to the details of production, innovation and growth for their tastes. Extending financialization and asset values is what they "understand" to be in the interests of financial intermediation and asset holders, while the actual needs of supply side production were, and continue to be, ignored. Raising demand and sorting out bank balance sheets was more important even although the fundamental theory justifying this is flawed.

Monetarism has delivered a trail of disasters over the last century starting with the 1929 New York Crash and the Great Depression. Certainly Friedman's repeated assertion that money supplies cause inflation "

in the long run" always was absurd but as we have exceeded any long run since he made such statements, and quantitative easing has soaked the economy in money, he has been shown to have been completely wrong. In 1976, RIO-Real Incomes Objective research showed that inflation is a direct result of price setting decisions by companies and is not connected to monetary policy.

4Why no one asked Carney why the Bank of England, throughout his reign, maintained an inflationary target of 2% to 2.5% as a policy objective, when this translates into a 20% devaluation of the purchasing power of the currency, in a decade of increasing income disparity and rising poverty, is a mystery.

1 Hector McNeill is the Director of SEEL-Systems Engineering Economics Lab.

2 "

Development Economist Gerald M. Meier Remembered", Graduate Schoool of Business, Stanford University, 2011.

3 McNeill, H. W.,

"A Real Money Theory II"4 The slumpflation crisis (rising prices and unemployment) in the 1970s/1980s was caused by cost-push inflation linked to rapidly rising international prices of petroleum. The knee jerk monetarist reaction was to associate inflation with excessive "demand", so interest rates were raised to high levels causing widespread home repossessions and further economic depression. Under quantitative easing, the massive release of funds, associated with close-to-zero interest rates was "designed" to raise "demand", but this act destroyed the income from savings of millions of people, depressed the economy and placed housing prices beyond the reach of millions.

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2020) unless otherwise indicated