RIO and Bitcoin

Hector McNeill1

SEEL

RIO-Real Incomes Objective and Bitcoin are both decentralized mechanisms designed to maintain the value of the currency. RIO is a fundamental change in the policy framework and policy instruments that make use of the standard currency subjected to different regulations. Bitcoin is a fundamental change in the means of exchange as an alternative currency, and its management.

This article reviews how both are designed to operate to the same end. They are not competitive but complementary. What remains in question is whether the existing central bank functions and centralized monetary policies can survive. It is of course important to identify who benefits from such changes.

|

Location of RIO and Bitcoin with respect to conventional economic "schools"RIO-Real Incomes Objective policies arose as a result of economic analysis and development work initiated in 1975. The motivation at that time was that neither monetarism nor Keynesianism possessed any policy instruments to address slumpflation (the combination of rising unemployment and inflation). Any "solution", applying conventional centralized policy instruments which imposed interest rates, tax rates and money volumes based on debt, only exacerbated the state of affairs for the majority of constituents. Although this policy impasse was caused by slumpflation being cause by cost push inflation the work on RIO revealed the inoperative state of conventional policies to manage the economy to achieve real growth and a distribution of wealth and incomes.

Bitcoin is a cryptocurrency

2. There is no available information on when the concept development was initiated but a paper appeared in 2008 entitled, "

Bitcoin: A Peer-to-Peer Electronic Cash System", produced as an anonymous person or group of people using the name "Satoshi Nakamoto". However, this was not a hoax because the group made the system operational by releasing its source code as open-source software in 2009.

Like RIO, One of Bitcoin's objectives is to arrest the erosion in the value of the currency by introducing algorithms and mathematical procedures that slow up the rate at which Bitcoins can be identified by Bitcoin miners up to a pre-established number issued of 21 million. Already in 2020 with around 18.3 Bitcoins "mined" and in circulation it is becoming marginally more expensive to unearth the remaining 1.7 million Bitcoins because the number of iterations required has become exponential so the marginal increase in energy used in processes is increasing, slowing up the process. By 2011 the value of a Bitcoin was around $0.30 rising to $998.00 by 1 January 2017. Today (mid-2020) the value of Bitcoins is around $9,300.00

Basic similarities and difference between RIO and Bitcoin

The similarities between RIO and Bitcoin relate to their common decentralization agenda. Both RIO and Bitcoin have a fundamental objective of arresting the decline in the purchasing power of the currency which results from the use of increasing money volumes via additional exogenous money. The result is always the debasement of the currency. However, how they achieve this is quite different.

RIO maintains the currency unit of exchange but makes use of a range of policy instruments all of which have the objective of removing the role of centralized interest rates and exogenous money growth based on debt to control inflation and "economic growth" based on the Aggregate Demand Model". A considerable amount of evidence has been gathered under the RIO development programme to explain how monetary policy debases the currency as a direct result of centralized on-size-fits-all policies (See

"The emerging status of Modern Monetary Theory" ). Other versions of RIO policies eliminate corporate taxation to terminate the strong differential that exists between corporate profits and wages and which causes income disparity by arresting wage rates while promoting asset holder inflation-base but real incomes growth for asset holders. This is designed to reverse the prolonged assignment disparity marked by profits steadily rising as a share of GDP and wages steadily falling as a share of GDP during the last 35 years. RIO's characteristics which eliminate centralized impositions to "manage" demand can be characterized as decentralizing. On the other hand, RIO arms individuals and corporate groups with business rules geared towards increasing the investment environment by promoting sustainable production and services delivery based on productivity enhancements. The incentives that encourage higher productivity investment also encourages moderated and even reduced unit output prices. As a result, the outcome is rising real incomes for both work groups and consumers. Whereas RIO can operate in parallel with conventional monetary policy and central banks it would be more effective if conventional policies were abandoned and central banks were closed.

Bitcoin's approach to countering the debasement of the currency is different from RIO because it aims to provide an independent alternative to the existing currency ass a medium of exchange. Bitcoin is issued by those who participate in its mining, holding or using it in transactions and the only relationship to central banking is that because at the moment Bitcoins are not used for all transactions it needs to be converted into national currencies and therefore works alongside central bank issued currencies. The approach can be characterized as providing individuals with the "liberty" to transact without any reference to central government currencies other than in relation to the exchange rate when users wish to use the values they hold for other things. Bitcoin, being operated by individuals has not concentrated on monetary policies but rather "go round" them. Because of its independent character governments and central banks have been unsure as to the likely impact of Bitcoin on monetary policy in general. Incipient regulations have been introduced and some states and countries have established Bitcoin-friendly frameworks such as the Isle of Man and Wyoming State in the USA where Bitcoin companies can operate. There is a literal geographic split between Bitcoin mining set ups and companies dealing with transactional aspects. Bitcoin mining, which is increasingly energy intensive, is tending to be located where electrical energy costs are low and many are ending up in remote locations with renewable energy generation grids and which are lower priced. An added benefit of this migration is that most energy used, around 87%, is from sustainable renewable sources. On the other hand, friendly transactional Bitcoin environments such as Wyoming State and the Isle of Man do not have competitive energy sources, so this locational split between the two types of service persists.

ApplicationThe software for users of Bitcoin is not user friendly and many consider this to be a major barrier to a more widespread use. There is still a need for Bitcoin management applications that possess adequate security to prevent online hacking and stealing of Bitcoins as well as ease of use. In spite of this Bitcoin is becoming a product/service of growing significance in countries with poor economic condititions and debasement of currencies as well as for international trading transactions. User benefits include instant transfer with exceptionally low commissions.

In the case of RIO, there is a lack of reference to RIO by "mainstream economists" because it does not fit the conventional configuration of "accepted" understanding economic theory. This is because all conventional policies including, monetarism, Keynesianism, supply side economics and Modern Monetary Theory and all based on the Aggregate Demand Model. This rejects the basis for Say's Law largely because Say's Law does not accommodate exogenous money based stimulation of growth. However, it is the exogenous money aspects that debases the currency.

Gaps in the Bitcoin approachThe basic issue facing a future with Bitcoin is the questions of income and wealth distribution. At the moment all of the attention is on the crypto-technology and increasing value of the Bitcoin linked to the slower Bitcoin extraction rates in spite of rising mining hash rates

. For Bitcoin to end up with a realistic "price discovery" process it needs to cover an increasing proportion of transactions in an economy. However to relate all of this to income distribution and real incomes of wage earners is where the RIO policy framework comes in.

Important RIO-Real Incomes Objective policy development contributionsThe development work output of RIO

established that inflation is not caused by money volumes as far back as 1976. However, the constant reference to the Quantity Theory of Money by monetarists was also demonstrated, by RIO analysis, to be flawed because of missing variables. These were savings and assets. RIO therefore substituted the QTM by the Real Money Theory (RMT) in 2020 (See

"A Real Money Theory" and also

"The real incomes component of the Real Money Theory - A note" ). The RMT demonstrates how exogenous money does not flow principally into goods and service market sectors but, rather, into assets. Any inflationary impact is principally in asset markets. This is self-evident under quantitative easing as well as the current super-charging of land, real estate and corporate share prices as a result of central banks releases; especially by the Federal Reserve in the USA.

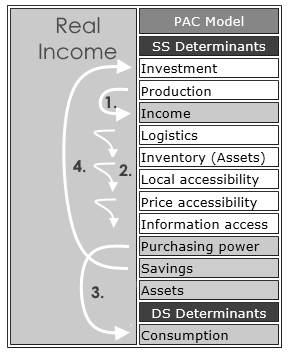

This demonstrates that the Aggregate Demand Model, deployed by all conventional policies, do not work as promised or even as explained by economists. In order to explain how the economy works it is important to start with a Say's Law model and this has been developed by RIO development output as the Production, Accessibility and Consumption Model (PACM) which parallels Say's Treatise on Political Economy of which the sub-title was, "

On the production, distribution and consumption of wealth". The PACM is described elsewhere in articles on this site but basically if exogenous money is not being imposed on an economy all income is earned from production units for goods and services, and consumption, the size of which is related to the transfer of funds into incomes by production units. So what is consumed to satisfy needs or "demand" is all supply side generated. Under these circumstances the only way to increased real incomes and ensure equitable distribution is to enhance productivity by changing the way things are done, refining methods and investing based on savings i.e. money generated endogenously, from within the supply side. The other essential factor is that wages should increase roughly in proportion to increased productivity which usually reduces operational unit costs. As a result this combination of factors enhances the purchasing power of the currency resulting in a general rise in real incomes or the worth of wages and profits. This condition is known as a

positive systemic consistency which changes distribution from a zero sum game to one where all participants gain.

Integrating innovations in policy and units of exchangeThe interesting state of affairs concerning RIO and Bitcoin is that if they were somehow integrated this would provide a powerful policy framework for a rapid expansion in Bitcoin and a return to a macroeconomy that would be transparently supporting the interests of the majority. On the other hand RIO and Bitcoin can operate together with no coordination simply because they are both decentralized models with the same objective but in ways that are complementary. Because the approaches cover different elements in the macroeconomic framework components, they are not going to bump into each other operating in the same economy. RIO and Bitcoin operating separately or together will however, bump into conventional central bank based monetary policies.

In terms of economic logic and the track record of monetarism, RIO and Bitcoin are on the side that offers most potential benefits for the majority of constituents.

Innovation in the face of an archaic mindsetRIO and Bitcoin represent important innovations in policy options and a medium of exchange. They both face an archaic monetarist mindset established centuries ago by those who held decision-making power such as royalty and those upon whom royalty depended for money, rich merchants and business people. Therefore this plutocracy, government by the rich, was in operation long before there was anything approaching representative democracy. Monetarism has consolidated the power of modern plutocrats as an asset owning class of individuals who today, even although we now have "universal suffrage", continue to influence the decisions on economic and monetary policy. The constituency continues, as in past centuries, to have no say in these decisions. The notion of "public choice" and a more constitutional economic framework is not something they wish to contemplate. However, the track record is there to see as a disaster unfolding because economists and politicians continue to uphold archaic and flawed theory and promote unworkable policies, as far as the majority of constituents are concerned. Politicians and economists are not appealing to sound economic logic in their promotion to their policies with regard to the interests of the majority of contemporary constituencies made up of voters, but are rather follow the pathways of the obsequious since, in the end they are also wage earners very dependent for their status and roles on the plutocrats.

1 Hector McNeill is the Director of SEEL-Systems Engineering Economics Lab.

2 "

36th Annual Review of Global State-of-the-Art Network Technologies", Chapter 25, "Bitcoin", SEEL, 2020.

3 For a detailed historic review, up to the present day, Saifedean Ammous' book, "

The Bitcoin Standard - The decentralized alternative to central banking", 286pp, Wiley, provides an excellent analysis in the first 100 pages of this book which provides many examples of the inevitable instability and disasters resulting from growth in "exogenous money".

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2020) unless otherwise indicated