Assets, savings, cash and expenditure distortions under quantitative easing

Hector McNeill1

SEEL

This week (6th January, 2020) data was released (High Pay Centre) that showed that many executives of companies earn the equivalent of the average national annual salary within a week of work. Some secure that income within three days.

This is a direct result of financialisation what has gathered pace over the last 30 years, culminating with the 2008 financial crisis.

Unfortunately the current government policy is only exacerbating the income disparity problem and there appear to be no plans to change policy. This indicates that the government is in favour of the creation of a social class rift based on income disparity. This is contrary to the rhetoric of a "one nation government".

|

Central Banks - the elephants in the room

The failed policy of QE has been promoted and implemented by the leading Central Banks (European Central Bank, The Bank of England, The Federal Reserve) and this has been a serious error leading to an impasse. The impasse is the practical difficulty of extracting the economy from a state of declining investment, productivity and real wages by relating interest rates to natural or reasonable levels to encourage beneficial savings and investment levels. However, QE has set interest rates at such low levels that reversing this policy through increased interest rates could result in another financial calamity because of the excessive levels of debt generated under QE.

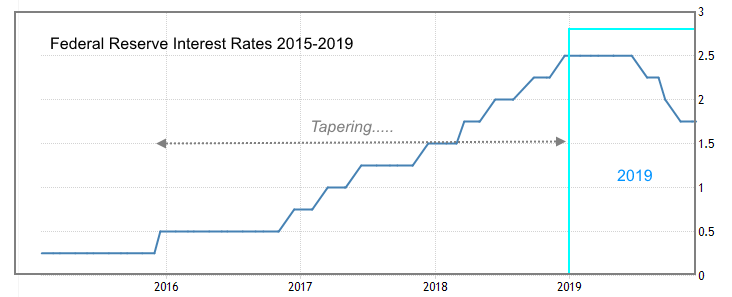

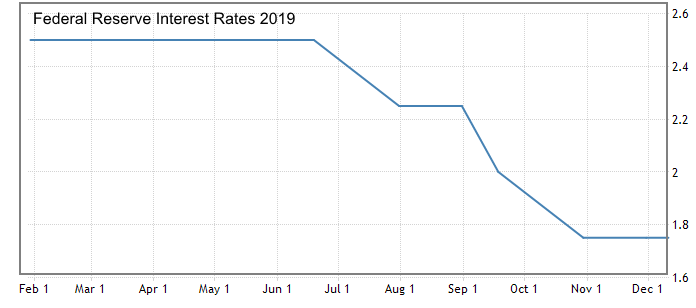

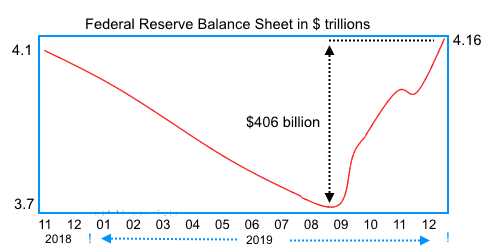

One or more banks in the USA are already facing difficulties as indicated in the overnight or Repo market being particularly active in helping out distressed banks. |  |  |  | The crisis is essentially a global one and it calls into question the very utility of central banks. Their stated independence has not avoided a serious imbalance by having increased the growth in low interest debt, favouring banks, at the expense of income parity amongst the people of the countries they are supposed to serve. Federal Reserve - leading the pack of Central Bank lemmingsAfter attempting to "taper" QE during 2019 by increasing interest rates to 2.5% the Federal Reserve (FR) gave up in September 2019 due to distress in the banking sector and reduced the rate in steps to 1.75%. In less than 4 months the FR issued some $406 billion sustaining the US assets bubble. 60% of the stock market rise over this period is attributed directly to this FR QE action in this period, unrealetd to corporate performance or prospects - a mirage.  |

|

|

|

Quantitative easing (QE) was introduced in response to the failure of the banking system as a result of sector incompetence and exposure to poor loans that were the result of a lack of due diligence and in many cases criminal activity.

QE was essentially a "solution" drummed up by the banks themselves to be able to use public funds to recover from a self-imposed disaster. This move killed the savings opertions supporting pensioners living off fixed income returns based on interest. Here the free market and justified bank failures were substituted by a bail out of those responsible for poor practice by lowering the official interest rate and encouraging lending (debt based on monetary expansion). Banks used the low interest money to favour their own interests and those of large corporate clients to purchase assets and thereby draining the consumer/real economy of funds by locking the majority of the expanded money supply up in assets such as real estate, land and stocks and shares whose values were blown up by share buy backs.

This has been combined with the tail end of the largest and hidden privatization of land worth around Ł400 billion involving the transfer of public land holdings into the hands of a select group of private "asset holders". This was initiated following Margaret Thatcher's commitment to privatisation and continued under the New Labour Blair regime and subsequent Conservative governments ever since. This has involved over 2 million hectares of land or 10% of the British land mass. Estimates of the private rentier incomes derived from these transferred assets is somewhere in the region of $20 billion each year which is also inflation-proof, unlike people's wages. As a result the rate of land and housing rental growth has outstripped most of the growth figures lowering the real incomes of those who need to rent. Increasing numbers cannot afford a house purchase as a result of land hoarding or land banking by construction and house building companies who have restricted the numbers of lower cost housing. Some of this land was released from publicly held assets, such as rail, water and national health holdings for the private sector to make "better use of the land for housing" but contrary to this policy of privatisation, this land has been hoarded and not used for housing. This is yet another example of the government's preference for helping expand the rentier economy benefiting a small community based on the accumulation of assets whose value rises over time. At the same time the differential impact of this process has been a lowering of relativbe real incomes of others in his country, exacerbating the income disparity problem.

The mechanics of what is mentioned above is described in the following articles and notes:

Is there such a thing as a natural interest rate? - noteOptions manipulation ruining corporate performance - a noteWhy quantiative easing undermines the constitutionIt's assets, stupid!The outcome of quantitative easing on real incomes - summary note

In summary the government is not supporting a free market in monetary transaction interest rates but chooses to intervene centrally by fixing the interest rate leading to a demarkation between those who benefit from the stated rate and those who do not. As always, such centrally administered, non-free market top down policies, create winners and losers. In the current circustances there are more losers than winners. This has been the case for some time and yet the government continues with this policy.

The track record of Central Bank operations and government policies based on "monetary principles" have served to disprove the theory upon which policy decisions are based, the so-called Quantity Theory of Money (QTM). Somewhat like Keynesianism being unable to manage the slumpflation of the 1970s-1980s, The QTM provides no solution to the current low interest rate low real income crisis created by policy apparently being guided by the flawed logic of QTM. In reality it is unlikely that QE was motivated by any QTM logic (which does not exist anyway) but rather by the strong Central Bank private banking lobby interests wishing to cut their losses by receiving a bail out from government; QE became the window dressing for the appearance of a monetray policy which has failed because it has exacerbated income disparities in this country.

In spite of an outward air of confidence the Central Banks are driving the economy towards a calamitous situation which will end up with extreme dificulties for the economy in the form of failing companies unable to clear debt for lack of productivity and significant to mass unemployment. In the case of the United Kingdom the government needs to explain what the strategy is to head off this potential crisis. This policy continues as the country prepares to leave the European Union a decision that will impose additional economic difficulties on the country. So far there is little evidence that there is a full understanding of what is required on the part of the government which apparently intends to continue to impose the same failing policy on the country. This continues to exacerbate income disparity, and cannot be considered to support any notion of "one nation governance".

1 Hector McNeill is the Director of SEEL-Systems Engineering Economics Lab.

|

|

|

|