A constitutional economic policy - Part 7

Designing a sustainable future - Step 1

Hector McNeill1

SEEL

Moving out of the current economic crisis, as was the case in the 1970s and 1980s under slumpflation, requires changes in the procedures and methods for selecting investments to emphasize their contribution to price performance and competition rather than solely looking at nominal profits. This is because the policy instruments and the results of their application do not in fact "manage demand" but rather depress real incomes of the constituency whose aggregate disposable income creates the actual levels of aggregate consumption. This calls for changes in the microeconomic techniques for unit price setting to augment the real incomes of all associated with economic units.

As is self-evident, monetarism and Keynesianism never made much of a contribution to the necessary supply side management decisions. Between, 1990 and 2020, these macroeconomic policy frameworks and regulations have created a strong disincentive for this type of growth strategy.

This article is the first of three (3) that describe the steps required for an economic recovery process:

- Identifying the investments offering the most rapid returns for growth

- Establish an agreed policy that supports company actions to invest in higher productivity configurations based on transparent business decision analysis procedures able to accommodate the range of conditions facing each economic unit

- Establish clear incentives and business rules to ensure alignment of corporate and macroeconomic policy objectives

The objective is a marked increase in efficiency to drive the economy forwards with substantive gains in real incomes growth and distribution,

The broader background analysis to requirements will be presented in the forthcoming "British Strategic Review" to be published Q4 2020 (see box below). |

BackgroundGovernments have seldom demonstrated an ability to pick winners even although this is what they have done increasingly, since the early 1980s, by imposing a mix of centrally planned interventions in a mix of Keynesian and monetarist policy instruments which have boosted the welfare and incomes of the winners who, overall have been in the form of asset holders and financial institutions while gradually prejudicing the real incomes of an increasing proportion of the constituency, whose main source of income is wages. As a result, what has been supposed to be "demand management", has ended up undermining this very notion.

| What is the point of attempting to advance one's condition by investing in education, a project, or dedicated work, when economic policies depreciate opportunities, undermine productivity and destroy real income prospects? |

|

|

|

BSR was organized to analyse strategic issues facing the United Kingdom. A decade of increasing turmoil resulting from inappropriate economic policies, BREXIT and Covid-19 demands fresh in-depth analysis of the economic and constitutional challenges facing the nation, with a focus on recovery.

The Q4 2020 volume reviews the issues and presents a series of economic and constitutional proposals for a sustainable future. |

|

|

Macroeconomic environments need to be redesigned to eliminate tendentious impositions as a result of market interventions, in money supplies and to impose base rates for interest. These introduce differential impacts on companies according to their particular circumstances, an imposed and inequitable treatment of economic actors. The close to zero interest rates have prejudiced savers and those relying on fixed incomes while the same policy has previously imposed very high interest rates causing many to lose their homes as a result of repossessions.

Policy needs to accommodation of the very different conditions of every constituent and economic actor by removing restrictions on the ability of each to take decisions to advance their interests while, at the same time, preventing any such activities from impeding the ability of others to do the same. The current macroeconomic policies fail to achieve this simple constitutional requirement, giving rise to the current and past financial crises.

The constant increase in money volumes and low interest rates is not increasing "demand" as policy makers predicted. A decade of quantitative easing (QE) has become a case study proving that the theoretical link up between money volume and "demand" doesn't exist. Such a poorly design policy did not have to wait for QE to discover this fact. This was pointed out by the analyses completed under the real incomes approach in 1976. Japan's experience with QE, since the 1980s, has created a zombie economy and John Maynard Keynes pointed this out many years before. It is illogical and therefore pointless to persist in the application of this impractical economic theory. Government ministers, the Bank of England decision makers and professional economists, who persist in supporting such a poorly designed policy, need to be required to justify such decisions when the evidence, since 1975 has consistently pointed to failure. The common referral to the Quantity Theory of Money (QTM) died out rapidly as the central justification for monetary theory when the real incomes policy work exposed why, even on theoretical grounds, the QTM identity does not even carry reference to the main variables at play (see,

"A Real Money Theory").

There is also an outdated notion that how government allocates funds from the public purse has a direct impact on productivity and growth. There is very little evidence to support this notion because, once again, it assumes governments can pick winners, in the sense of identifying actions to "grow the economy" but which in practice generate some employment but no significant gains in productivity or real economic growth. This challenge to "pick winners" also applies to the inability of governments to discriminate effectively between multiple proposals for R&D funding, for example. Centrally-funded research and development initiatives often support those who prepare convincing proposals but the grounds upon which assessors of proposals can determine whether or not proposals and under or over-ambitious in terms of potential achievements and time lines, often end up as political decisions. The former defence research and development initiatives were a very expensive way of subsidizing certain firm's activities through subcontracts to essentially support the development of capabilities of interest to the military sectors. Throughout this process the central objective tended to be towards innovations that provided military strategic advantage with spin-off becoming commercialized civilian applications. The process of releasing such advances, from the grip of military control on security grounds, has been in many cases too prolonged.

|

There was an opportunity in the early 1990s, with the economic collapse of the Soviet Union, for the UK to have taken a more effective advantage of what was called the "peace dividend" and pioneer alternative sustainable growth technologies. But this valid foundation for expanded civilian research and development programmes was resisted by aerospace companies linked to armaments because the former military orientation gave them more leverage and indeed money. The idea of spreading this research money amongst many companies with a commercial civilian orientation was not effectively supported and since that time R&D investment has slowly declined, reaching a total of around 1.69% of GDP in 2019 (see box on left). This is an exceptionally low figure given that the quality is bound to vary significantly and the transition between R&D through prototyping to new beneficial commercial application time frames are not well analyse and reported, so any attempts to calculate potential cost-benefit of R&D will be on shaky ground.

With the transitions in funding of universities following the 1980s and the growth in student debt finance, there has been a significant financialization impulse that has resulted in many R&D activities are being used primarily as sources of income for staff with the objective of any fast effective delivery of results from R&D filtering through into applications that create economic growth, being coddled along to maintain income flows. In terms of a basis for a national technological strategy, this is an unacceptable state of affairs.

TOC, the theory of constraints, identifies physical resources, market conditions, modes of thought and policies pursued, to be the main constraints on desired progress.

When economic paradigms are wrong, policies fail. Markets lose potency and the prospects of all are greatly diminished. |

|

|

There is also a question of the quality of R&D in terms of relevance to the needs of the economy and the actual quantitative economic returns on this investment. In economies with larger manufacturing sectors, the generation of pointers on needed areas of applied research is more active and generally new procedures, arising from applied R&D, transfer more rapidly into beneficial applications. Where applied R&D encounters knowledge deficiencies then basic R&D activities benefit from the identification of relevant useful feedback to orientate their activities in directions of direct future relevance to the economy.

Therefore, the across-the-board comparison of the percentage of GNP allocated to R&D in different countries, does not provide much information of relevance to gaining any insight of the quality of R&D and its potential contribution to the solution of issues of economic significance.

The growth of financialization and the size of corporations dealing in derivatives and commercial investment led to a change of focus to shareholder value during the period 1980 through 1990s and away from productivity enhancing investments in the UK.

Adapted from "Investing in UK R&D", The Royal Society, The British Academy, Royal Academy of Engineering, The Academy if medical Sciences, May, 2019. |

There was a definite strategy on the part of corporations to substitute of UK-based labour by offshore engineering in South East Asia employing very low income work forces. With returns rising as a result of offshore engineering serious R&D fell into a trap of being regarded with short-sighted cynicism by many businessmen who were more intent on maximizing short term returns from their offshore operations.

The significance of shop floor innovationHowever, many offshore engineering contracts for production and mounting of devices possessed clauses allowing shop floor process improvements and some R&D in the production plants in offshore locations. What was not fully understood, by those making the financial investment decisions, was that much innovation arises as a result of learning to solve issues and to improve shop floor processes. As a result, over the last 30 years, most production know how and associated tacit knowledge has migrated from the UK to South East Asian production plants and their staff. The natural consequence of shop floor operations being associated with changes to improve productivity, the teams involved develop important insights into how a product design could improve the efficiency of production. The result of this gradual process of human assimilation of competence is reflected in the fact that China today leads the world in the registration of more high tech patents than any other country. Overall, the flows of investment funds into R&D in the UK is well below needed levels, not only because of poor decisions based on finance, but, more importantly, it is the result of the significant loss in productive capacity in manufacturing and a significant growth in service activities.

InvestmentThe annual levels of business capital investment across all sectors is around £200 billion each year. This is substantial amount of money. A logical strategy is to create incentives for companies to fine tune the allocation of these funds to increase the proportion of investments that maximize:

- The rate of substitution of current processes by better performing state-of-the-art substitutes

- Operation of process innovation circles at company and across sectors to further improve overall organizational and technical performance

- Gains in productivity

- Optimizing trade-offs between cross-elasticities of employee income consumption impacts, productivity rises and feasible unit prices

- Competitive price setting

- Business expansion

- Human resources training in current and new business processes

- Feasible import substitution and exports

|

The basics of productivity

A common basis for calculating the expected return on an investment is cost-benefit analysis (CBA) which compares the present values of expected cash flow streams of input costs and income, over a period including the investment set up and operational phases. Invariably the conditions upon which a CBA is calculated such as input prices, market conditions and other factors change during the course of implementation. As a result the prices of inputs and outputs remaining at the values sleeted and used in the CBA calculation generally change. Therefore the actual return realized is often not the same as the CBA used to justify an investment.

Because we are interested in identifying investments that will maximize the economic growth and recovery paths it is logical to attempt to identify those investments that will generate the fastest growth recovery and help raise employment. We also need to be aware that, as stated, conditions invariably change during implementation. This reality refers to uncertainty and therefore economic policies need to permit companies to take rational decisions, under conditions of uncertainty, to maximize returns under changing conditions, as opposed to attempting to deliver the original plan whose CBA is based on conditions that no longer exist.

Because change affects all companies in different ways because they have different inputs, use different technologies and sell into different markets, centralized policies that set fixed values for policy instruments, such as interest rates and money volumes, cannot be effective and are very inefficient and lack effective traction. Conventional policies provide no decision making rules or methods on how each company should react to the unique circumstances facing each company. Policy needs to be able to provide a general incentive, that is applicable under any circumstance, while allowing each company to maximize their evolution in productivity and investment returns. Policy's objective should be to help move the productivity levels at the microeconomic level upwards so as to generate economic growth at the macroeconomic level. This can be achieved on the basis of a three step procedure:

- Identifying the investments offering the most rapid returns for growth

- Establish an agreed policy that supports company actions to invest in higher productivity configurations based on transparent business decision analysis procedures able to accommodate the range of conditions facing each economic unit

- Establish clear incentives and business rules to ensure alignment of corporate and macroeconomic policy objectives

STEP 1. Identifying the investments offering the most rapid returns for growth

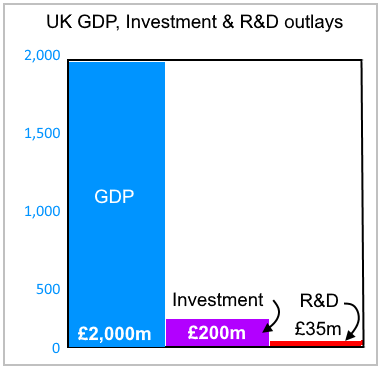

The diagram on the left shows that in the roughly £2 trillion GNP UK economy, there is an annual investment of around £200 billion, or 10% of the GDP, in investment and £35 billion, or 1.7% of the GDP, in R&D.

As things stand in this diagram there are two investment options, capital investment and R&D. Because the R&D is not broken down into basic research and categories of applied research these figures are somewhat amorphous and not particularly useful from the standpoint of investment strategy decision making targeting maximized growth. In spite of this many leading organizations advocating increased investment in R&D from the current figure of 1.7% to 2.4% of GDP is somewhat speculative in terms of working out what the potential returns to the economy are. There is a need to accelerate growth by selecting investments according to funds available and the expected return time line that determines the CBA.

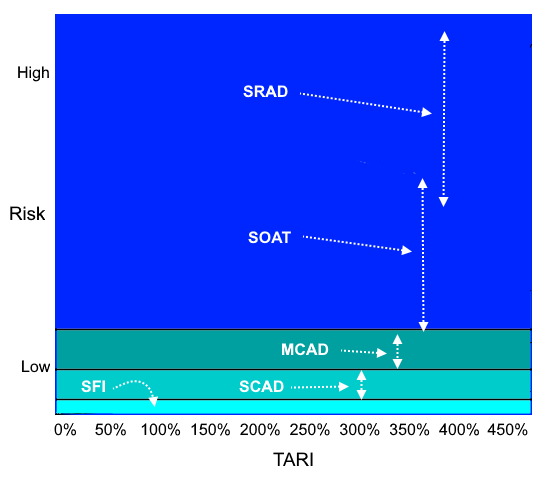

Usually, what is referred to as Shop Floor Innovation (SFI) has an almost immediate impact on productivity of existing systems. There can be slight delays caused by time to "reorganize" new layouts of production lines or to adjust to new techniques, but an assumption can be made that the impact can be delivered and measured within days or up to 6 months. Introducing State-Of-the-Art Technologies (SOAT), the more usual basis for investment, requires procurement delays, set up, commissioning and personnel training phases and a sometime prolonged period for operations to come up to full capacity operation. Overall this investment cycle can take anything between 1 and 5 years. Between capital investments (SOAT) and R&D, there is a class of investments in applied research which can be divided into Short Concept to Application Development (SCAD) and Medium Concept to Application Development (MCAD). SCAD results can be expected within 12 months and MCAD results might take between 1 and 2 years. Conventional R&D can be classified as Speculative Research & Development (SRAD) where results are expected in over 1-10 years since there is usually no firm time line for delivery of knowledge relevant to applications with any impact on productivity.

These types of investment are presented in the table below.

Expanded range of investment options embracing identified applied development projects

| Type of investment | Impact time scale | Nature |

| SFI - shop floor innovation | <6 months | incremental |

| SCAD - Short concept to application development | <12 months | spaced |

| MCAD - medium concept to application development | <24 months | spaced |

| SOAT - state-of-the-art | 12-60 months | blocky |

| SRAD - research and development (speculative) | 24 to 120 months | more spaced |

In 1974, Stan Sadin, A NASA researcher defined a scale for multi component technological development referred to as TRL-technology readiness levels.

It is a technique to reduce applied development risks associated with multi-

component technology systems starting at basic research through to operational systems. |

|

|

Decision AnalysisThe advent of decision analysis as a logical quantitative basis for taking decisions based on quantitative methods advanced during the 1960s, largely by the Decision Analysis Group, under the leadership of Ron Howard of the Stanford Research Institute in Menlo Park. As a university taught discipline it took on variants at the Engineering School at Stanford University under Professor Ron Howard and on applications systems engineering under Professor Bruce Lusignan. However, it is revealing that in terms of understanding the significance of technological maturity to design investment strategies it was only in 1974 that NASA formerly adopted the proposal by Stan Sadin to introduce what was referred to as "TRL-technology readiness levels" which is self-explanatory. The objective is to reduce risk by ensuring that technology is ready to be applied, having gone through the normal proof of concept, prototype testing and approvals.

Although this is a basic decision analysis concept it is notable that this has not been applied to the UK government's referral to R&D where there is no detailed run down of how close R&D and applied development activities are to delivering something that can be used by economic actors as an investment component. It is not altogether clear how well qualified the "research institutions" including academia are to complete such an analysis in an objective fashion because of the political nature of their funding processes; however, this is something that needs to be carried out.

What follows, is a way to break down this lack of transparency to move towards a more useful analysis of the potential contributions of the vast array of "developments" and "state-of-the-art" technologies and techniques to enhancing productivity and economic growth.

SFI - Shop floor innovationAlthough SFI is often not regarded as investment the operation of process innovation circles at company level and across sectors to further improve overall organizational and technical performance can result in major continuous gains in productivity and learning. A large part of the foundation of South East Asian advances in high technology innovation in production and design is fertilized by shop floor innovation. Major benefits from SFI as a source of productivity include:

- usually very low cost because it often involves incremental changes

- continuous improvement and physical productivity increases

- development of human capabilities

- development of processing system design competence

- development of product design competence in relation to more efficient manufacture

- continuous incremental reductions in time used and waste reduction

- development of product design competence in relation to more efficient manufacture

- production yield rises and unit cost reductions

SCAD - Short concept to application development

SCAD is more complicated that SFI in that it is part of applied research and development. However it usually is oriented to the solution of a well-defined need and can require the development and testing of prototypes applying the process approach consisting of short design-implementation-testing-analysis cycle, followed by design adjustments and a repeat of this cycle. SCAD becomes more commonly used in reasonably mature production processes and service work forces where the tacit knowledge based on operational experience is advanced so that adjustment to prototypes are very practical leading to a relatively short and successful development periods. SCAD often involves modest amount of funding and can dovetail into SFI in cases of slightly more ambitious innovations. The benefits from this source of productivity include:

- usually modest costs and relatively low risk involving slightly larger changes than SFI

- stepwise improvement and physical productivity increases

- development of human capabilities

- development of processing system design competence

- development of product design competence in relation to more efficient manufacture

- continuous incremental reductions in time used and waste reduction

- development of product design competence in relation to more efficient manufacture

- production yield rises and unit cost reductions

MCAD - Medium concept to application development MCAD is usually a larger scale SCAD and also part of applied research and development. Its is also oriented to the solution of more complex but well-defined issues that usually require prototype development or test reconfigurations to existing operational structure. These are usually best tested in computer-based decision analysis models that complete quantitative simulations before money is spent on implementing change. MCAD is also likely to be more commonly used in reasonably mature production processes and service work forces where the tacit knowledge based on operational experience is advanced so that adjustment to prototypes are very practical leading to a relatively short and successful development periods. MCAD takes longer as a function of complexity of the solution and like SCAD can dovetail into SFI developments but would usually require more funding than SCAD. The benefits from this source of productivity include:

- usually lower costs than SOAT capital investment relatively low risk involving slightly larger changes than SCAD

- larger step improvement and physical productivity increases

- development of human capabilities

- development of processing system design competence

- development of product design competence in relation to more efficient manufacture

- continuous incremental reductions in time used and waste reduction

- development of product design competence in relation to more efficient manufacture

- production yield rises and unit cost reductions

SOAT - State-of-the-art technologiesState-of-the-art technologies are often the basis for new capital investment. In 2020 a ball park figure for this investment was £200 billion but there is little data on its locational-state with regard to its position on the state-of-the-art best practice range. All that can be emphasized is that investors need to carry out an adequate decision analysis in selecting the most suitable investment in the trade-off between price and characteristics of the potential productivity gains.

SRAD - Speculative research and development Conventional R&D can be classified as Speculative Research & Development (SRAD) where results are expected in over 1-10 years since there is usually no firm time line for delivery of knowledge relevant to applications with any impact on productivity.

Ranking of productivity gains and returnsMoving beyond the establishment of the most likely time frame within which any particular development can be used as an investment component, is the decision as to which developments can bring about the highest economic and financial impact in the shortest time. This is a critical refinement because sometimes the most impactful investments are very low cost and generate a very high return in terms of productivity. The larger an investment, in terms of financial resources, the higher the commitment risk. This risk is not necessarily associated with the amount of funds committed but rather with the uncertainties introduced by a range of necessary activities associated with required stages in the investment cycle involving a larger range of different people and competence levels and all of which involve their own time cycles. SEEL's experience in investment projects shows that a lack of due diligence applied to large projects can result in failure. The events and procedures that cause failure are not related to the basic structure of the investment blue print of how the final product will function. They relate to the design process not taking into account many administrative procedural delays, all of which are predictable and quantifiable, but also because macroeconomic policies create significant constraints on operations causing final performance results to be far below the "original plans". In many cases this has led to project cancellation and a waste of resources, time and effort. Risk is reduced by using operationally proven technologies or scheduling investment according to critical paths with realistic floats (allowances for pre-determined time estimate variations) on those investments which offer the highest short term return.

Getting the concept of return rightThe economy is made up of a highly differentiated and heterogeneous mix of land, individuals and ranges of available technologies and techniques. The mix of appropriate output in an economy is guided by the choices made by constituents through the expenditure of their disposable incomes. This "endogenous" money volume circulates throughout the supply side of the economy where demand, that is, consumption, is established by the aggregate incomes paid to those employed in the economy. Growth in the economy, during the period 1945 through 1965 was largely obtained as a result of savings from endogenous money, leading to investment in more productive activities resulting in more output being shared and paid for. As a result of moderated or reduced prices constituents, whose nominal incomes did not rise appreciably, experienced significant rises in their real incomes as a direct result of increased productivity and accessible prices. As a result the standard of living rose significantly during this period, the same was true in the USA (See

The real incomes and investment trap).

Prior to 1929, and since 1975, the economic model is a stark division of economic factors into just land, labour and capital as the inputs to a primitive Aggregate Production Function (APF) where variations in inputs result in different outputs. For several years this was represented in academia by the Cobb-Douglas model. However, the Aggregate Demand Model, is a financialization of the APF. In this model production or output is encouraged or discouraged by varying the volume of money through "exogenous" or externally-generated funds, in the economy and setting base interest rates. As a result, the APF model became a three factor Aggregate Demand Model (ADM) of natural resources (substituting for land), labour and finance (substituting capital). This ADM approach to policy possesses no policy instruments to allow constituents or economic units to maintain any coherence between the number of people employed, and who earn income from their contribution to output and the rise in productivity, previously created by companies from savings and investment in appropriate technologies and techniques. Margins were withdrawn into "profits" and "financial assets" and the labour force, the conduit of money flows into consumption, or demand, became increasingly marginalized as a result decisions based on financialization principles and the growth in offshore engineering.

The current model continues to confuse capital for finance with capital in the form of technology and techniques. It is technology and techniques that hold the solution to increased economic growth and not exogenous money. Quantitative easing (QE) has demonstrated just how the financial dominance over macroeconomic policy decisions based on the simplistic and flawed Quantity Theory of Money has only diverted funds from real investment in appropriate technologies and techniques. What is accumulating is not a system distributing real incomes to the constituency, but a system that continues to concentrate financial capital assets in the hands of a few. As a result of the declining real incomes of constituents, the supply side flow of endogenous funds are becoming depleted because increasing amounts are leaking into assets through share buy backs while the prospects for outcomes of investments, under such policy-imposed market conditions, do not hold out much promise. This is why the price earnings ratios for shares have risen beyond levels of financial sustainability (See

The real incomes and investment trap); Covid-19 has exacerbated this state of affairs.

TARI-Time adjusted return impactPeter Schumpeter once defined profits as the guarantee of future activity and of employment (See,

The Profit Paradox). However, macroeconomic policy has failed to uphold constitutional objectives of protecting the freedom of constituents and companies to pursue their objectives while

Decision analysis applying TARI

Investments grouped by time-based impact delivery

Therefore risk independent of productivity impact |

preventing these activities from preventing others from doing the same. Policy has created structural barriers to the ability of constituents to exercise their freedom of action by causing a decline in their real incomes and by augmenting the time required for them to maintain their real incomes. Beyond that the only option left is debt. At the same time policy has encouraged a small faction of the constituency to reduce the freedom of constituents by reducing pay and extending hours of work as well as causing many to lose their employment through the movement of activities offshore. Innovation by many companies is not in reality innovation but rather take-overs through mergers and acquisitions, secured on the basis of financial incentives to all involved. Thus, "investment" is very much concerned with larger companies removing competition by buying their operations. This sort of "investment" does not advance the levels of state-of-the-art technologies and innovation. Profits have transitioned into value of capital assets held as opposed to the Schumpeterian sense of a guarantee of future activity and employment. This decadence of a constitutional model has been made possible by the constituency, in general, never being afforded the opportunity to make any contribution to decisions on monetary policy in a country that considers itself to be a democracy.

Investment decisions need to be based on criteria that balance the flow of endogenous money into consumption (demand) by encouraging rises in productivity through a range of possible investments while concentrating on short to medium term high returns so as to minimize risk and the need for debt. This leads to the concept of time adjusted return impact (TARI) which extends the notion of technology readiness to a

maximization of short to medium term rises in physical productivity (see graph right).

Therefore the initial step is to place emphasis on gains in physical productivity and economic input/output relationship or gross margin gains without initially changing the overall employment structure. The table below shows the types of data required in order to establish a rational basis for decision analysis. In terms of productivity some generic technologies, such as information technology, produce productivity gains of in excess of 1000% but depending upon the specific location in a process in a specific sector the impact can be reduced significantly on, for example, an automation process. The paradoxical and interesting issue is that although IT is generic in terms of its data processing logic, the required integrated configurations of that logic can vary significantly according to the application. Most sectors can benefit significantly from a broader applications of SOAT whereas in each case SFI, SCAD and MCAD usually offer far higher short to medium term rates of productivity increase at lower risk.

The required adjustments to financial results and the assignment of resulting cash flows is explored in the next article covering Step 2: Establish an agreed policy that supports company actions to invest in higher productivity configurations based on transparent business decision analysis procedures able to accommodate the range of conditions facing each economic unit. Step 3 will describe how the RIO-Real incomes objective policy macroeconomic instruments provide clear incentives and business rules to ensure alignment of corporate and macroeconomic policy objectives to ensure a more equitable distribution of real incomes and sustained economic growth.

Expanded range of investment options ranking short to medium lower risk and priced investments by time

| Type of investment by process by sector | Time adjusted return impact distributions |

| Type of investment | Impact time scale | Nature |  |

| SFI - shop floor innovation | 6 months | incremental |  |

| SCAD - Short concept to application development | 12 months | spaced | |

| MCAD - medium concept to application development | 24 months | spaced | |

| SOAT - state-of-the-art | 12-60 months | blocky |  |

| SRAD - research and development (speculative) | 24 to 120 months | more spaced | |

1 Hector McNeill is the Director of SEEL-Systems Engineering Economics Lab.

All content on this site is subject to Copyright

All copyright is held by © Hector Wetherell McNeill (1975-2020) unless otherwise indicated