Solving the PPR Puzzle

Hector McNeill

SEEL

During 1981 and 1982 I completed the first validation of the Real Incomes Approach by publishing a monograph1 entitled "Price Performance Fiscal Policy - A Real Incomes Approach". This was a summary of the work completed in 1976. I sent this to various people requesting an assessment and comments. One of the people I sent the document to was Professor Robin C. O. Matthews2, the then Master of Clare College Cambridge. In 1980, he had succeeded Brian Reddaway as Professor of Political Economy.

I eventually met Professor Matthews to discuss my proposals. He had obviously read and understood the document and considered that the model could tackle inflation. However, he expressed concern with the fact that my original preoccupation with solving the Slumpflation issues had meant that my model was biased towards that specific state of affairs, that is, where input prices and unemployment were rising. He concurred that the model appeared to squeeze inflation out of the system at the level of transactions. This being achieved through a Performance Levy (PL) on profits and salaries, whose level was set by the Price Performance Ratio (PPR). The practical issue pinpointed by Robin Matthews was to put me on the spot with a very simple question, "How does this work if input prices fall." I did not have an immediate reply. On reflection this was an obvious oversight on my part. He was very diplomatic and suggested I try and resolve this aspect of the model before the next validation.

Solving the PPR puzzle

It is interesting to observe how setting out to resolve a specific pressing issue can cause one to end up with tunnel vision. In economics, of course, this will not do because economic determinants are moving in all directions and therefore models need to be able to accommodate all eventualities. The too often heard ceteris paribus in economics is sometimes taken to absurd lengths. The need to gradually abandon the state of ceteris paribus to creep back to reality has been described by Alfred Marshall3. I finally worked out a solution which thanks to Professor Matthews' prodding helped me end up with a model that is more comprehensive and practical; however, no doubt able to benefit from further refinement. Indeed, on reviewing "real" economic data, especially in commodities, food, fibre and feedstocks, it is evident that we are talking about price trends since under "inflationary or deflationary conditions" we can witness a considerable oscillation in prices within any "trading period" for wide range of inputs.

For those who are curious the solution is set out below.

The formula for the PPR can be generalized to take as the "pointer" the direction of travel of unit input values. If these are positive, that is, rising, or negative, that is falling the objective of the PPR is to monitor the response of output prices to the recorded changes in input prices. The purpose of the PPR coefficient is therefore to see by how much output unit prices rise in response to input price rises with lower rates of unit output price rises reducing the upward pressure in prices. In the case of unit input value declines there is an interest in seeing by how much unit output prices fall in response to indicate the degree to which benefits are passed on.

As mentioned above the "lead" is taken by the direction of travel of input unit values. Thus there are two sets of PPR equations. One for rising unit input values and one for falling unit input values.

Inflation

Thus under inflationary conditions the degree and direction in which a company influences price inflation is the Price Performance Ratio (PPR). The PPR can be measured as the ratio of the percentage increase in unit output prices to the percentage increase in total unit input values over a given period of time:

PPR = (100(dPo)/Po)/(100(dPi)/Pi)

PPR = (dPo .Pi)/(dPi.Po) ..... (1)

where:

dPo is the increase in unit output prices during the period and Po is the unit output price at the beginning of the period;

dPi is the increase in total input values per unit during the period and Pi is the unit input value at the beginning of the period.

This was the "original" formula I proposed for the PPR in 1976 that was designed to tackle inflation and this was published in the 1981 monograph.

Deflation

Thus under deflationary conditions the degree and direction in which a company influences prices can be measured as the ratio of the percentage fall in unit input costs to the percentage fall in unit output prices over a given period of time. Note that this is the inverse of the equation 1 above and it is therefore of the following form:

PPR = (100(dPi)/Pi)/(100(dPo)/Po)

PPR = (dPi .Po)/(dPo.Pi) ..... (2)

where:

dPo is the decrease in unit output prices during the period and Po is the unit output price at the beginning of the period;

dPi is the decrease in total input values per unit during the period and Pi is the unit input value at the beginning of the period.

Desirable & Undesirable States

The PPR provides an indication of the degree to which the supply chain individual firm activities impact real incomes as a result of the summation of unit input costs (transacted) and the unit output prices (transacted). This occurs across a transformation process including: input procurement (transaction), external input logistics, internal input logistics, transformation process, internal output logistics (product or services), product sales (transaction), external output logistics (product or services) and delivered product or service.

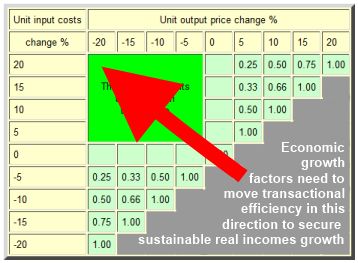

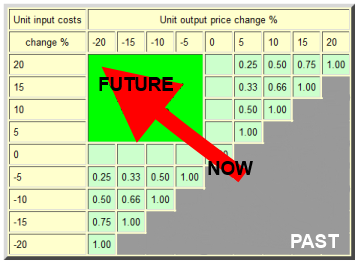

Innovation target zonesWith current technology, techniques and accumulated tacit knowledge, there is a frontier beyond which we cannot operate with state of the art technology. For example if unit input costs rise by 20% it would normally be difficult to secure a 20% reduction in unit output prices without losing a considerable amount of money. However, through re-adaptations of state of the art, systems engineering and rational decision analysis it is possible to redesign processes and maximize process throughput so as to carry the evolution of technological and economic performance to enter the innovation target zones leading to a significant rise in supply side-generated real income as a result of lower unit prices and market penetration. The innovation target zones, desirable and undesirable states are shown in the table below.

Price Performance Ratios (PPRs)

associated with different unit input value movements & movements in unit output prices

| Unit input costs | Unit output price change % |

| change % | -20 | -15 | -10 | -5 | 0 | 5 | 10 | 15 | 20 |

| 20 |

This area represents

the innovation

target zone | 0.00 | 0.25 | 0.50 | 0.75 | 1.00 |

| 15 | 0.00 |

0.33 | 0.66 | 1.00 | |

| 10 | 0.00 | 0.50 | 1.00 | | |

| 5 | 0.00 |

1.00 | | | |

| 0 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | | | | |

| -5 | 0.25 | 0.33 | 0.50 | 1.00 | | | | | |

| -10 | 0.50 | 0.66 | 1.00 | | | | | | |

| -15 | 0.75 | 1.00 | | | | | | | |

| -20 | 1.00 | | | | | | | | |

Innovation target zone | | Desirable states | | Undesirable states | |

|

This table provides a map of the distribution of likelihoods of sources of enhanced real incomes. However, the extent of real income generation at the macroeconomic level can only be estimated by applying sector demand schedules for local and regional markets. In the case of global markets, the elasticity of demand for price-setters is well above the market norm so the returns to lower PPR states are enhanced by market penetration, returns to scale, better procurement conditions and the accumulation of tacit knowledge leading to quantifiable increases in performance measured in terms of unit costs of production.

The PPR map is not only a useful guide to feasible attainment in terms of real income growth according to the sector/technologies but it also provides a map of targets for research and development and technology requirements. At all times these explicit descriptions will be improved, in practice, through the refinement of techniques, that is, the way people apply technology, achieved through practice and the further accumulation of tacit knowledge. The PPR map also provides an indication of the evolutionary transition of where we stand today in terms of the given past and the necessary future.

In the box, at the beginning of this article, there is a reference to Robin Matthews' findings on the UK eonomy post-war period, where growth could not be explained by Keynesian fiscal policy but the reason, he felt, lay in demand arising out of wartime destruction and an unusually prolonged private sector investment boom. Around the time of this publication, other more detailed studies, largely on the US economy, established that some 50%-60% of growth in primary, extractive, industrial, manufacturing and service sectors arises from learning, or supply side phenomena, including technology, learning, technique refinement and innovation. Learning and the accumulation of tacit knowledge are the most important contributors to growth.

Why the Real Incomes Approach is differentThe Real Incomes approach embraces such factors as important resources and makes use of them by influencing transactional behaviour to stimulate the proactive application of these growth factors. It is notable that the main conventional texts on Keynesianism, monetarism and supply side pay scant attention to these factors and as a result provide no basis for growth in their derived policies.

2 McNeill, H. W.,

"Price Performance Fiscal Policy - A Real Incomes Approach", Charter House Essays in Political Economy, HPC, December 1981, ISSN: 0262-0014 ISBN: 978-0-907833-00-4)

2 Robin Matthews was an Oxford-educated economist who spent most of his academic career as a member of the Cambridge Faculty from the early 1950s onwards. He moved to Oxford to take up the Drummond Professorship from 1965-1975, succeeding John Hicks, and returned to Cambridge as Master of Clare College from 1975-1993. In 1980, he succeeded Brian Reddaway as Professor of Political Economy. He returned to the Economics Faculty at the height of Mrs Thatcher’s enthusiasm for the monetarist views of Milton Friedman. Eager to ensure that undergraduates should be exposed to all schools of thought, even with those with which he disagreed, he gave a series of lectures which were pointedly entitled "Monetarism". These presented a balanced, if critical, exposition, remarkable for their prescience in stressing the distinction between the traditionalist views of Friedman himself, and the much more radical position (the precursor of ‘New Classical Economics’) that was being put forward by others.

3 Alfred Marshall (1842 – 1924) was one of the most influential economists of his time. His book, Principles of Economics (1890), was the dominant economic textbook in England for many years. It brings the ideas of supply and demand, marginal utility, and costs of production into a coherent whole. He is known as one of the founders of economics. In 1885 he became professor of political economy at Cambridge, where he remained until his retirement in 1908. His observations of ceteris paribus can be found in

"Principles of Economics",Book V Chapter V para V.V.10 where he describes the use of ceteris paribus as follows:

|

"The element of time is a chief cause of those difficulties in economic investigations which make it necessary for man with his limited powers to go step by step; breaking up a complex question, studying one bit at a time, and at last combining his partial solutions into a more or less complete solution of the whole riddle. In breaking it up, he segregates those disturbing causes, whose wanderings happen to be inconvenient, for the time in a pound called Ceteris Paribus. The study of some group of tendencies is isolated by the assumption other things being equal: the existence of other tendencies is not denied, but their disturbing effect is neglected for a time. The more the issue is thus narrowed, the more exactly can it be handled: but also the less closely does it correspond to real life. Each exact and firm handling of a narrow issue, however, helps towards treating broader issues, in which that narrow issue is contained, more exactly than would otherwise have been possible. With each step more things can be let out of the pound; exact discussions can be made less abstract, realistic discussions can be made less inexact than was possible at an earlier stage."

|

Updated: 23/06/2013 correction substituted word "employment" by "unemployment" in the second paragraph.